Are RMDs required if still working?

Individuals are required to take RMDs from most retirement accounts once they turn age 72. However, an exemption to the RMD rules – often referred to as the still-working exception – allows some people to delay RMDs until they retire.

Do I have to take an RMD in 2021?

However, in 2021 you will have to take your first RMD. This RMD is due by the end of 2021, not April 1, 2022. Since they won’t turn 72 until 2021, they won’t have to take their first RMD until April 1, 2022.

Yes, even if you continue working past age 72,* you have to take an RMD from your IRA. However, you may qualify for an exception from taking RMDs from your current employer-sponsored retirement account, such as a 401(k), 403(b), or small-business account, if: You’re still working.

What should I do if I’m over 70 and still working?

Required minimum distributions (RMDs) are government-mandated withdrawals from each of your retirement accounts, except Roth IRAs. Retirees must begin taking RMDs at 70 1/2, but you can delay RMDs from defined contribution plans, like 401 (k)s, if you are still working and own no more than 5% of the company you work for.

Do you have to make a distribution at age 70?

Also, if you are over age 70 1/2 and still working for the company, no distribution is generally required. There are some exceptions to this rule and some companies have different rules so check with your plan administrator. It’s generally easier to do a direct rollover into an IRA for simple distributions.

Can you take a RMD if you are still working at age 70?

Answer: No. All IRA owners (other than Roth IRA owners) must begin taking RMDs when they turn age 70 ½. This applies to traditional IRAs, as well as to employer-sponsored IRAs, like SEP and SIMPLE IRAs. Whether you are still working makes no difference. Question: If I am still working past age 70 ½, can I delay RMDs for my 401 (k)? Answer: Maybe.

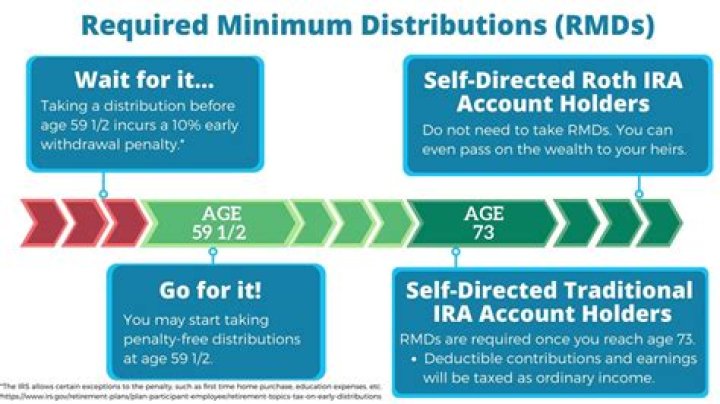

When do you have to take required minimum distributions?

Required Minimum Distributions (RMDs) generally are minimum amounts that a retirement plan account owner must withdraw annually starting with the year that he or she reaches 72 (70 ½ if you reach 70 ½ before January 1, 2020), if later, the year in which he or she retires.