Can a refinance closing be done electronically?

For a fully online closing, you can expect to meet remotely using a video conferencing app like Skype, Zoom, Google Meet, etc. Any payments that must be processed for closing will likely be done via electronic transfer and mortgage documents will have to be signed electronically.

When should I submit my mortgage application?

The best advice is to start the process of applying for a mortgage before you even start seriously looking for somewhere to buy. If you’re looking at properties before starting to arrange your mortgage, you’ve left it too late.

What is a refinance application?

A mortgage refinance refers to the process of getting a new loan for your home. When you refinance, the new mortgage loan pays off the old one, so you’re left with just one loan and one monthly payment. There are a few reasons people refinance their homes.

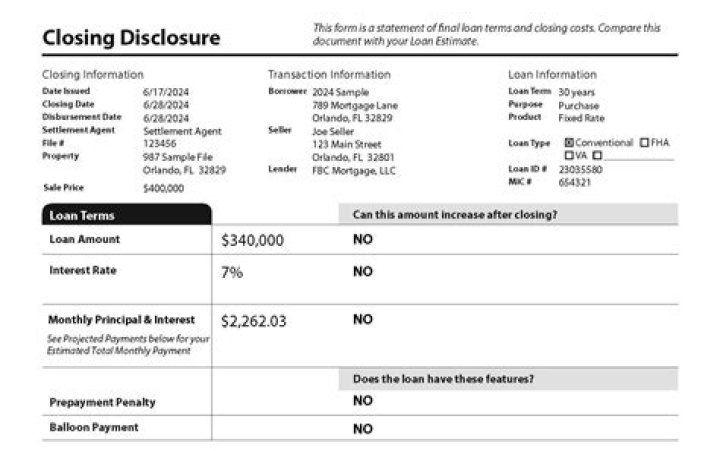

What documents are signed at a refinance closing?

Refinance closing documents often include:

- Final version of the closing disclosure statement.

- Your mortgage or deed of trust.

- Promissory note.

- Your right to cancel.

What happens after you sign closing documents for refinance?

Once documents are signed, they’ll be delivered to your lender for final review. If you’re refinancing to receive cash, know that those funds will not be available for another three days after signing. This is a result of the refinance right of rescission.

What happens after I submit my mortgage application?

After you submit your application, your lender does a credit check on you, and also does what’s called an ‘affordability assessment’, to make sure you can actually afford the mortgage you’ve applied for. They’ll also carry out a valuation survey on the property to make sure it’s worth what you’re paying for it.

How do I record a mortgage in QuickBooks?

From the QuickBooks Lists menu, choose Chart of Accounts. Right-click anywhere and click New. Create a loan account….Set up a mortgage

- From the Type drop-down list, choose Expense.

- Enter a name for the account (Interest, for example).

- Click OK.

Can a refinance be denied after closing documents are signed?

After Closing Although it’s rare, it is even possible for your lender to pull a refinance loan after closing. Whether in the beginning or end, reasons for a mortgage loan denial may include credit score drop, property issues, fraud, job loss or change, undisclosed debt, and more.

When should you close on a refinance?

You can refinance your mortgage loan to take advantage of lower interest rates, change your term, consolidate debt or take cash out of your equity. Though there is no exact time limit on how long a refinance can take, most refinances close within 30 – 45 days of your application.

What kind of expense is mortgage?

Interest expense captures the interest payments your company makes on its debt. Mortgage interest expense captures the interest payments made on any outstanding mortgages your company has, for example, for your company’s office building or warehouse.

How do I pay back a shareholder loan in QuickBooks?

To record a payment:

- Select + New.

- Under Suppliers, select Cheque.

- From the Account drop-down list, select the liability account you created for this loan.

- Enter the Amount of the payment.

- Select Save and close.

How do I categorize a mortgage in QuickBooks online?