Can Form 3115 be amended?

A Form 3115 can also be filed with an amended 2019 tax return or AAR if it is filed within six months of the original due date and follows the procedures outlined in Rev. Proc. 2015-13, section 6.03(4). Options may also exist to adjust for both 2018 and 2019 additions on its 2020 tax return.

Can Form 3115 be filed?

Taxpayers will still need to submit two copies of the Form 3115 to the IRS. Taxpayers must continue to file Form 3115 with their tax return (including extensions). However, instead of mailing the duplicate paper copy of Form 3115 to the IRS in Ogden, Utah, taxpayers can now fax it to 844-249-8134.

Can you take bonus depreciation on an amended return?

Generally, taxpayers can file an amended tax return for the property’s placed-in-service year to claim the bonus depreciation and adjust the depreciation allowable on the qualified property, provided that the amended tax return is filed before the taxpayer files its tax return for the first taxable year succeeding the …

Can you make an election on an amended return?

§ 280C(c)(1) and (c)(2), is precluded from making such an election on an amended return/claim for refund. The Code and the Treasury Regulations are clear; such an election may only be made on a timely-filed original return (with extensions). I.R.C.

Can you change from cash to accrual?

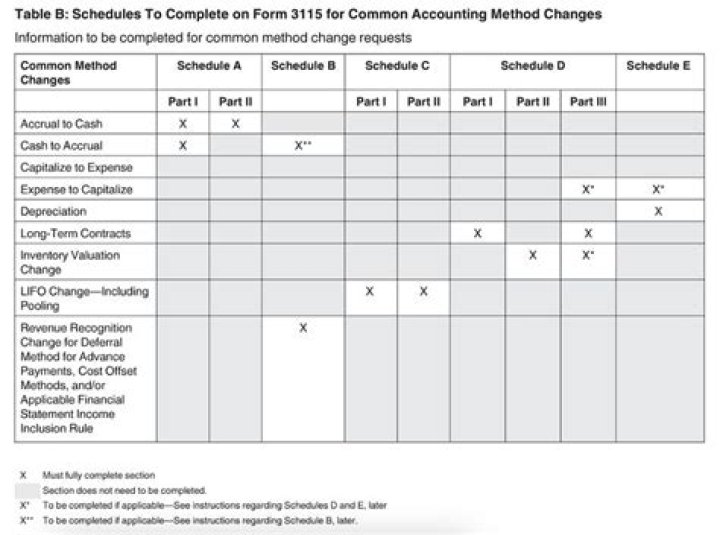

To convert from cash basis to accrual basis accounting, follow these steps: Add accrued expenses. This means you should accrue for virtually all types of expenses, such as wages earned but unpaid, direct materials received but unpaid, office supplies received but unpaid, and so forth. Subtract cash payments.

Does Turbo tax Support Form 3115?

If you are using TurboTax for your personal tax return, you need to MAIL your tax return to include Form 3115. It must be part of your tax return, PLUS you need to mail or fax a SECOND copy to the IRS.

How much is bonus depreciation in 2019?

For tax years 2015 through 2017, first-year bonus depreciation was set at 50%. It was scheduled to go down to 40% in 2018 and 30% in 2019, and then not be available in 2020 and beyond. The Tax Cuts and Jobs Act, enacted at the end of 2018, increases first-year bonus depreciation to 100%.

When can you switch from accrual to cash?

Accrual to Cash In general, companies with average annual gross receipts in the prior three years that are less than $10 million (less than $5 million for C corporations) can make an automatic method change to the cash method.

What is included in accrual to cash adjustment?

Conversion to the cash system requires one to subtract all the transactions recorded but not yet received or paid from the totals on the income statement. That means subtractions of all accrued expenses, including accrued tax liabilities and purchases, total accounts receivable, and accounts payable amounts.

How do I change from cash to accrual on tax return?

To convert to accrual, subtract cash payments that pertain to the last accounting period. By moving these cash payments to the previous period, you reduce the current period’s beginning retained earnings. Cash receipts received during the current period might need to be subtracted.

How many years does it take for a taxpayer to use an impermissible method of accounting before it is considered an adoption of the accounting method?

Depreciation Attributes Considered Accounting Methods If an impermissible method of depreciation has been reported for at least two consecutive years, then a change in accounting method would be required to correct any errors.

How do I amend 3115?

There are two methods of requesting change with a Form 3115. You can file in duplicate by attaching the original form to your federal income tax return. You also need to file a copy of the form with the IRS (Internal Revenue Service) National Office after the first day of the year.

How to prepare form 3115 for cash to accrual method accounting change?

You probably need to prepare Form 3115 for a cash to accrual method accounting change. Skip to primary navigation Skip to main content Skip to primary sidebar Evergreen Small Business Actionable Insights from Small Business CPAs Home Small Business FAQ Monographs Maximizing PPP Loan Forgiveness Preparing U.S. Tax Returns for International Taxpayers

Do you have to file a form 3115 with the IRS?

No user fee is required. An applicant that timely files and complies with the automatic change procedures is granted consent to change its accounting method, subject to review by the IRS National Office and operating division director. Ordinarily, you are required to file a separate Form 3115 for each change in method of accounting.

When to use a negative adjustment on form 3115?

Since the section 481(a) adjustment is the heart of Form 3115 for a change to the cash method of accounting, it is essential that all computations be correctly presented since the adjustment affects taxable income in the year of change. In the example presented above, you would recognize the entire $35,000 negative adjustment in the year of change.

How do I Change my accounting method for sec.481?

And you need to explicitly document and describe the accounting method change and the Sec. 481 adjustment amount using Form 3115. You first file one copy of the 3115 form with the IRS’s National Office (typically) and then after that you attach another copy of the Form 3115 to your tax return.