Can I file S Corp election late?

A late election to be an S corporation and a late entity classification election for the same entity may be available if the entity can show that the failure to file Form 2553 on time was due to reasonable cause. Relief must be requested within 3 years and 75 days of the effective date entered on line E of Form 2553.

How do I request a late S Corp election?

To do so:

- Attach Form 2553 to your current year Form 1120S, as long as the form is filed within three years and 75 days after the intended date of S-Corp election.

- Attach to a late-filed Form 1120S, which will be under the same time restrictions (three years and 75 days of intended S-Corp election date).

How late can S Corp election be made?

For a New Business A corporation or LLC must file an S-Corp election within two months and 15 days (~75 days total) of the date of formation for the election to take effect in the first tax year. Example: Your articles of formation was filed on August 21st.

Can you retroactively apply for S Corp status?

If a business has a reasonable cause for not filing Form 2553 on time, the IRS may approve the S Corp election retroactive to the start of the LLC’s or C Corporation’s tax year. The business owner must explain on Form 2553 why the filing was submitted late.

What is reasonable cause for filing Form 2553 late?

Two acceptable reasonable causes are that your company’s president, chief executive officer or similar responsible person neglected to file the election, or your corporation’s tax professional or accountant neglected to do so.

What is considered a late S corp election?

If a corporation fails to make a timely election, it is considered a “late S election” and it will not qualify as an S Corporation for the intended tax year. The consequences of a late S election or failing to file an S election can be severe.

How long do I have to file S corp election?

A corporation or LLC must file an S-Corp election within two months and 15 days (~75 days total) of the date of formation for the election to take effect in the first tax year.

What is considered a late S-Corp election?

Who is responsible for late filing of S Corp?

The company’s president, executive officer, or someone in a similar position, neglected to file on time. In some cases, this may also be the corporation’s accountant who failed to file an S-Corp election. The corporation or the shareholders did not know that advanced filing was required — or that they needed to file at all.

When do you have to elect s Corp status?

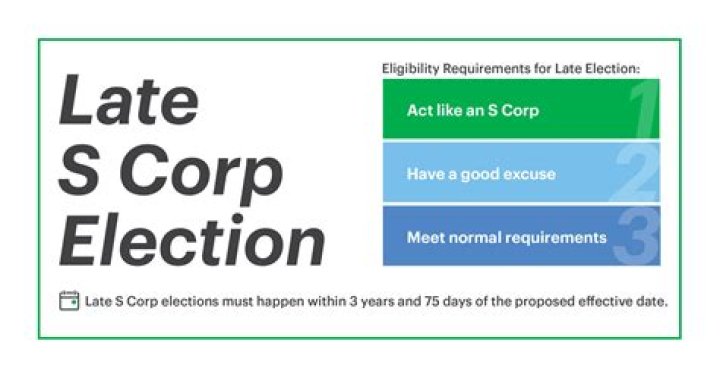

IRS Revenue Procedure 2013-30, effective September 3 2013, allows an entity to get relief and elect S Corp status within 3 years and 75 days from the date the election was originally intended to be effective. Holy cow. Three years! The IRS is basically saying that if you walk and smell like an S Corp, then you are an S Corp.

When to file a C corporation tax return?

For those LLCs who want to elect C Corporation status, it’s a little different. You need to file an IRS Form 8832 within 75 days of formation, or the first of the year. Unfortunately Form 8832s are always mailed in – there’s no fax or online method to get them taken care of at this time.

Is it possible to retroactively elect a s Corp?

Yes, you are able to engage in revisionist history and retro activate your S Corporation election to January 1, 2020, and have your income avoid a large chunk of self-employment taxes. Which year? Good question, and Yes, of course, it depends.