Can you refinance a condotel loan?

Loan To Value On Condotel Financing The maximum loan to value allowed is 75% LTV on purchase condotel mortgage loans and refinance condotel mortgage loans. Cashout refinance condotel mortgage loans are allowed up to a 75% LTV as well.

Can you get a mortgage on a condotel?

Yes, You Can Get Condotel And Non-Warrantable Condo Loans Rates typically run a half-percent higher than for a comparable conventional mortgage, and minimum downpayments start at 20 percent. Beyond that, however, getting an approval is simple.

How can I finance a non-warrantable condo?

Financing a Non-warrantable Condo One option is a portfolio loan, which is a loan that lenders keep on their books instead of selling. Portfolio loans can help buyers secure financing for non-warrantable condos, but they may have to meet stricter underwriting rules and pay a higher interest rate.

Are non-warrantable condos harder to sell?

Buying or selling a warrantable condo is similar to buying or selling a single-family home. Non-warrantable condos, on the other hand, aren’t as easy to buy or sell. These condos may look a lot like warrantable condos, but for one reason or another, Fannie and Freddie have deemed them too risky to buy.

How long must you pay mortgage insurance on a FHA loan?

11 years

While the law has changed more than once on this issue, current guidance states that borrowers who put down less than 10 percent on an FHA loan must pay for FHA mortgage insurance until the entire loan term is over. If you put down at least 10 percent, however, you can have FHA MIP removed after 11 years of payments.

Can I get a mortgage on a condotel?

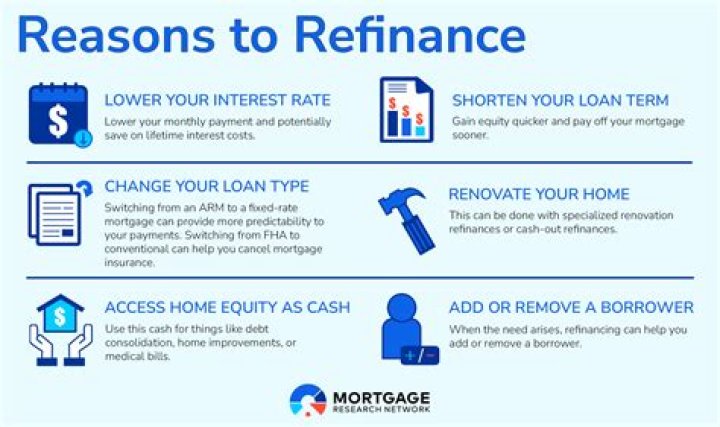

Can you refinance with nothing down?

More often than not, you don’t need to put down money to refinance your mortgage. For a cash-out refinance, on the other hand, there is no down payment requirement. Generally, lenders limit the amount you can cash out to 80 percent of the equity in your home.

What is condotel financing?

Condo Hotel Financing Overview A condo hotel (condotel) is a great way to own a luxurious vacation home without the traditional hassles of ownership such as property maintenance and finding renters when you’re not using it. Buying this type of property is similar to purchasing a typical condominium.

Where can I get a condotel purchase loan?

If you are interested in a condotel purchase loan or a condotel refinance mortgage loan please contact us at Gustan Cho Associates at 262-716-8151 or text us for a faster response. Or email us at [email protected] or visit us at

How does a refinance for a condo hotel work?

In the event, if the appraisal comes in lower than the anticipated estimate, the only way the condo-hotel refinance loan will go through is by paying down condotel mortgage balance so it falls within the 75% LTV on primary/secondary homes, and 60% LTV on investment homes Condo Hotel Financing is 30-year adjustable-rate mortgages: 3/1, 5/1. 7/1 ARM.

Can a condotel be financed through Fannie Mae?

Like non-warrantable condos, condotels cannot be financed through Fannie Mae or Freddie Mac and so, more often than not, condotel buyers have found themselves up a creek; ready to close but without suitable financing. Thankfully, mortgage money is available for condotels and non-warrantables — you just have to know where to look.

How does refinance to prepay work in real life?

You’re paying less interest because of your lower rate and your sending bonus principal monthly. When you refinance-to-prepay, your loan will “restart” to 30 years, but you’ll ultimately pay it off faster than had you never refinanced at all. It’s a math fact. Here’s a real life example of how refinance-to-prepay work.