Do 529 plans cover high school?

529 plans are considered tax-advantaged accounts. Savers can invest in the 529 plan, and the gains from the investments are free of capital gains, so long as the funds are used to pay for qualified expenses (which now include up to $10,000 of private elementary and secondary school tuition).

What if my child gets a full ride 529?

You don’t lose all or even most of your savings. It’s a myth that you’ll lost your 529 plan if the child wins a scholarship. A 529 plan offers tax-free earnings and tax-free withdrawals as long as the money is used to pay for qualified education expenses.

Can I use my daughters 529 for my son?

Parents can transfer 529 plan savings from one child to another without tax consequences by doing a plan-to-plan rollover or a beneficiary change.

Can you pay for a computer with a 529?

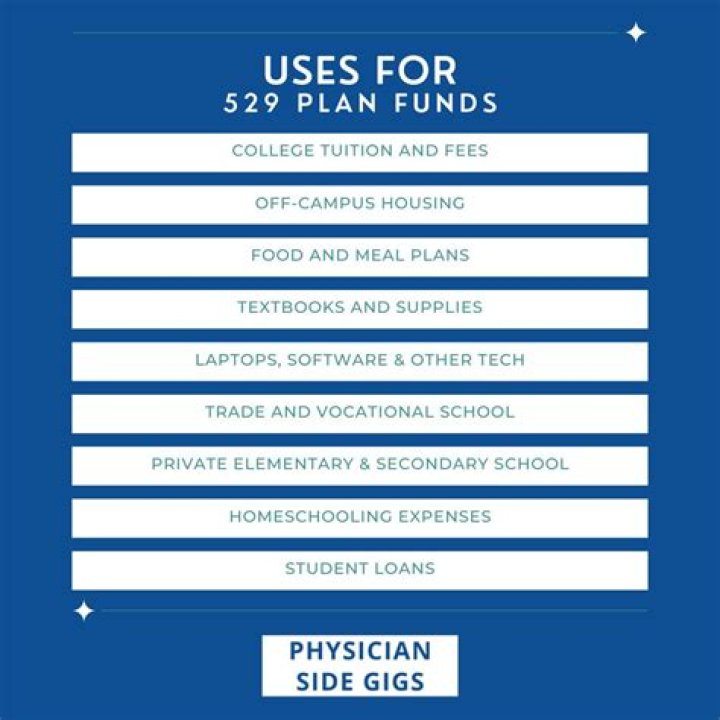

Since room and board costs are qualified expenses, that means students with an on-campus meal plan can pay for it with 529 funds. While some electronics such as computers are eligible expenses, these items must be required as part of the student’s attendance.

Can you borrow money from a 529 plan?

You can’t take out a loan against a 529 Plan You cannot take out a loan against the 529 account’s assets. When you take money from your child’s 529 Plan it is not a loan. You can’t borrow money from the account without also taking some of the earnings. Rather, you are making a withdrawal of both principal and earnings.

Can you roll a 529 into a Roth IRA?

The Internal Revenue Code does not permit a taxpayer to roll over a 529 college savings plan into a Roth IRA. Instead, one must take a nonqualified distribution from the 529 plan and invest the cash in a Roth IRA, subject to the applicable annual limits.

529 plans can be used for private elementary and high school tuition. The Tax Cuts and Jobs Act, which was signed into law in December 2017, allows families to use 529 plans to pay for up to $10,000 in tuition expenses at elementary or secondary public, private or parochial schools.

Can I use my 529 for private high school?

Rules on using a 529 plan to pay for private school In another words, The tax legislation in 2018 changed the federal tax treatment of 529 plans. More specifically, the provision allows families to use up to $10,000 per year, per child from a 529 plan to help pay for private school in grades K-12.

Should I use 529 money first?

The best bet is to use up the tax credits first, and then use the 529 funds on remaining expenses. To avoid penalties, make sure you withdraw money from the 529 in the same year it will be used for educational expenses. You will pay income taxes, but only on the capital gains.

Technology Items – You can use a 529 plan to cover technological needs such as computers, printers, laptops and even internet service. These items must be used by the plan beneficiary while enrolled in college.

What is the penalty for liquidating a 529 plan?

There is no penalty for leaving leftover funds in a 529 plan after a student graduates or leaves college. However, the earnings portion of a non-qualified 529 plan distribution is subject to income tax and a 10% penalty.

Is there a 529 plan managed by Fidelity?

For this and other information on any 529 college savings plan managed by Fidelity, contact Fidelity for a free Fact Kit, or view one online. Read it carefully before you invest or send money. 410286.32.0

Which is the best 529 plan for parents?

Age-based 529 plan portfolios appeal to parents who prefer to “set it and forget it.” They are a good place to start for parents who are new to saving and investing, since the investment risk is managed by the 529 plan.

How often should parents change investments in 529 plan?

Parents may make two 529 plan investment changes per year. With a shorter investment time horizon, parents of high school students should be more risk-averse when selecting 529 plan investments.

Can a fidelity account be used to plan for college?

Fidelity customers can plan for college as part of this comprehensive financial tool. Not a Fidelity customer? Use this tool to see if you’re on track to meet your college savings goals.