How are credit shelter trusts taxed?

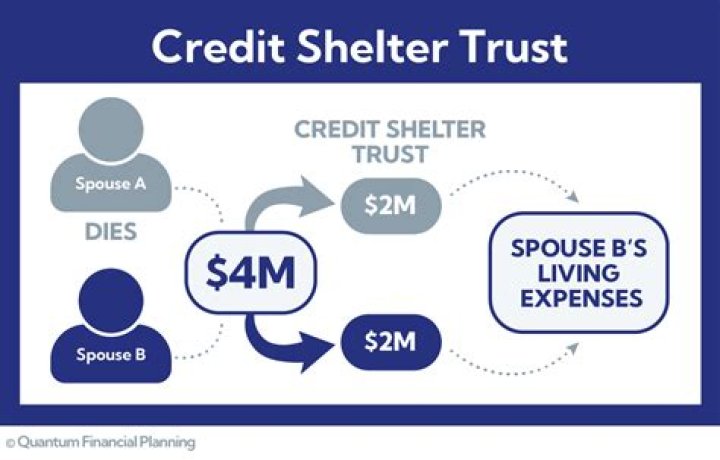

A credit shelter trust (CST) is a trust created after the death of the first spouse in a married couple. Assets placed in the trust are generally held apart from the estate of the surviving spouse, so they may pass tax-free to the remaining beneficiaries at the death of the surviving spouse.

Is a credit shelter trust revocable or irrevocable?

The trust is revocable, and the grantor can change its terms at any time during their lifetime. It becomes an irrevocable trust when the person dies and assets, typically what remains of the estate tax exemption, go to the trust.

Can you use a trust as a tax shelter?

Trusts can shelter assets from going through probate, or the legal process that happens after a person’s death in which the courts handle the payment of debts and taxes, and distribute remaining property according to the will or state law.

Is a disclaimer trust the same as a credit shelter trust?

The disclaimer trust functions essentially as a credit shelter trust, with assets not being included in the surviving spouse’s estate at his or her death. Second, the disclaimer trust can be structured in a manner to prevent creditors of the surviving spouse from making claims against the disclaimer trust.

Why would you use a disclaimer trust?

A disclaimer trust is a clause typically included in a person’s will that establishes a trust upon their death, subject to certain specifications. This allows certain assets to be moved into the trust by the surviving spouse without being subject to taxation.

Can surviving spouse be trustee of disclaimer trust?

The surviving spouse can serve as the sole trustee, but cannot have any power to direct the beneficial enjoyment of the disclaimed property unless the power is limited by an “ascertainable standard.” This is necessary both to qualify the disclaimer and to avoid any taxable general power of appointment.