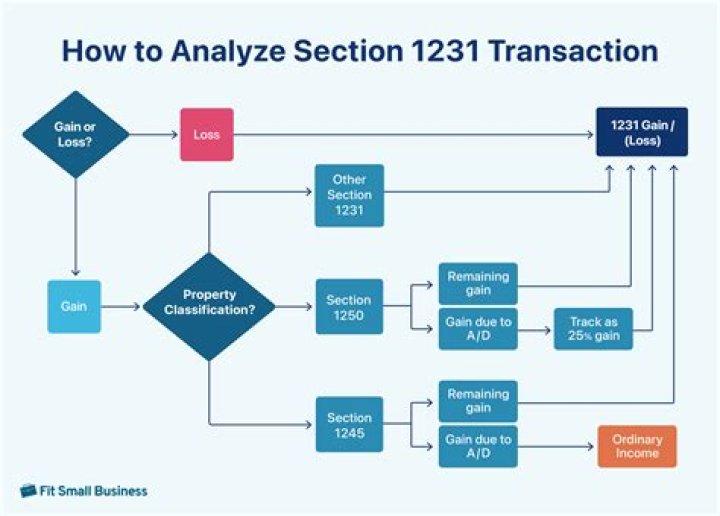

How are net losses treated in the section 1231 netting process how is a net section 1231 gain taxed?

If the netting process results in a net loss, section 1231(a)(2) specifies that the gains and losses shall not be treated as gains and losses from sales and exchanges of capital assets; therefore, the individual gains and losses are treated as ordinary gains and losses.

Are section 1231 losses deductible?

The Section 1231 Tax Advantage A net section 1231 loss is fully deductible as an ordinary loss. In contrast, a capital loss is only deductible up $3,000 in any tax year and any excess over $3,000 must be carried over to the next year.

What is Section 1231 Gain Loss?

Section 1231 property is real or depreciable business property held for more than one year. A section 1231 gain from the sale of a property is taxed at the lower capital gains tax rate versus the rate for ordinary income. If the sold property was held for less than one year, the 1231 gain does not apply.

Is rental property 1250 or 1231?

Commercial real estate, residential investment properties, buildings and land used for business are all section 1231 properties. Section 1250 of the Internal Revenue Code deals with depreciation on section 1231 property.

What is a net section 1231 loss?

10282: Section 1231 Loss “If you have a net section 1231 loss, it is ordinary loss. If you have a net section 1231 gain, it is ordinary income up to the amount of your nonrecaptured section 1231 losses from previous years.

What is Code section 1231 property?

Section 1231 property is real or depreciable business property held for more than one year. Examples of section 1231 properties include buildings, machinery, land, timber, and other natural resources, unharvested crops, cattle, livestock, and leaseholds that are at least one year old.

Is furniture a 1231 property?

It should because all 1245 property is 1231 property. Specifically, section 1245 property examples include all depreciable and tangible personal property, such as furniture and equipment, or other intangible personal property, such as a patent or license, which is subject to amortization.