How do you calculate fixed overhead volume variance?

It is calculated as (budgeted production hours minus actual production hours) x (fixed overhead absorption rate divided by time unit), Fixed overhead efficiency variance is the difference between absorbed fixed production overheads attributable to the change in the manufacturing efficiency during a period.

How do you calculate volume variance?

To calculate sales volume variance, subtract the budgeted quantity sold from the actual quantity sold and multiply by the standard selling price. For example, if a company expected to sell 20 widgets at $100 a piece but only sold 15, the variance is 5 multiplied by $100, or $500.

How do you calculate fixed MOH?

A common way to calculate fixed manufacturing overhead is by adding the direct labor, direct materials and fixed manufacturing overhead expenses, and dividing the result by the number of units produced.

How do you calculate fixed and variable overhead variance?

The formula for the calculation is:

- Overhead Cost Variance:

- (2) Fixed Overhead Variance.

- or St.

- = Actual hours worked x Standard variable overhead rate per hour – Actual variable overhead.

How do you calculate variable overhead variance?

Formula of Variable Overhead Efficiency Variance

- VOCV=

- VO Expenditure Variance= (Actual Total Time *Standard Rate Per Hour)- (Actual output * actual rate per hour)

- VO Efficiency Variance = (Actual output* Standard Rate Per unit)- (Actual hour* Standard Rate Per hour)

What is the volume variance?

A volume variance is the difference between the actual quantity sold or consumed and the budgeted amount expected to be sold or consumed, multiplied by the standard price per unit.

How do you find volume variance and rate?

These three calculations can be represented by the following formulas:

- Rate Var = (Actual Rate – Budgeted Rate) * Actual Average Balance * Basis.

- Volume Var = (Actual Avg Bal – Budgeted Avg Bal) * Budgeted Rate * Basis.

- Mix Var = (Actual Rate – Budgeted Rate) * (Actual Avg Bal – Budgeted Avg Bal) * Basis.

How do you calculate fixed manufacturing overhead budget variance?

The fixed overhead budget variance – or the fixed overhead expenditure variance – is calculated by subtracting the budgeted costs from the actual costs. As an example, assume the budgeted overhead costs for one month total $10,000.

What is fixed variable overhead?

Fixed overhead costs are constant and do not vary as a function of productive output, including items like rent or a mortgage and fixed salaries of employees. Variable overhead varies with productive output, such as energy bills, raw materials, or commissioned employees’ pay.

What is a volume variance?

How is the fixed overhead volume variance calculated quizlet?

The fixed-overhead volume variance can be determined by SUBTRACTING APPLIED fixed overhead from BUDGETED fixed overhead. Applied fixed overhead = Predetermined fixed-overhead rate x Standard allowed hours.

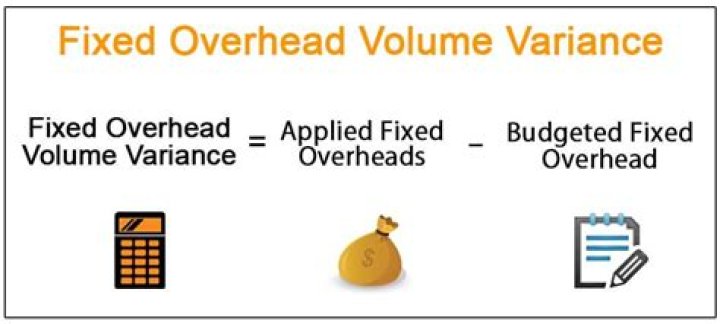

What is the formula for fixed overhead volume variance?

The formula of fixed overhead volume variance is given below: Fixed overhead volume variance = Budgeted fixed overhead – Fixed overhead applied Fixed overhead volume variance = Fixed component of predetermined overhead rate × (Budgeted hours – Standard hours allowed for actual production)

What is the efficiency variance for fixed manufacturing overhead?

There is no efficiency variance for fixed manufacturing overhead because, by definition, fixed costs do not change with changes in the activity base. The fixed overhead volume variance is solely a result of the difference in budgeted production and actual production. The fixed overhead production volume variance

What is the difference between fixed overheads and fixed overhead volume?

Fixed Overhead Expenditure Variance: the difference between actual and budgeted fixed production overheads. Fixed Overhead Volume Variance: the difference between fixed production overheads absorbed (flexed cost) and the budgeted overheads. Under marginal costing system, fixed production overheads are not absorbed in the cost of output.

What is the fixed overhead total variance in absorption costing?

In case of absorption costing, the fixed overhead total variance comprises the following sub-variances: Fixed Overhead Expenditure Variance: the difference between actual and budgeted fixed production overheads. Fixed Overhead Volume Variance: the difference between fixed production overheads absorbed (flexed cost) and the budgeted overheads.