How do you calculate real WACC?

WACC is calculated by multiplying the cost of each capital source (debt and equity) by its relevant weight by market value, and then adding the products together to determine the total.

How do you convert nominal WACC to real WACC?

There are two approaches to dealing with the conversion of a nominal post-tax WACC into a real, pre-tax WACC. One is to gross up the nominal post-tax WACC to a nominal pre-tax WACC by applying the estimated tax rate (36%) and then de-escalating this nominal pre-tax WACC using an estimated inflation rate.

How do you calculate market return for WACC?

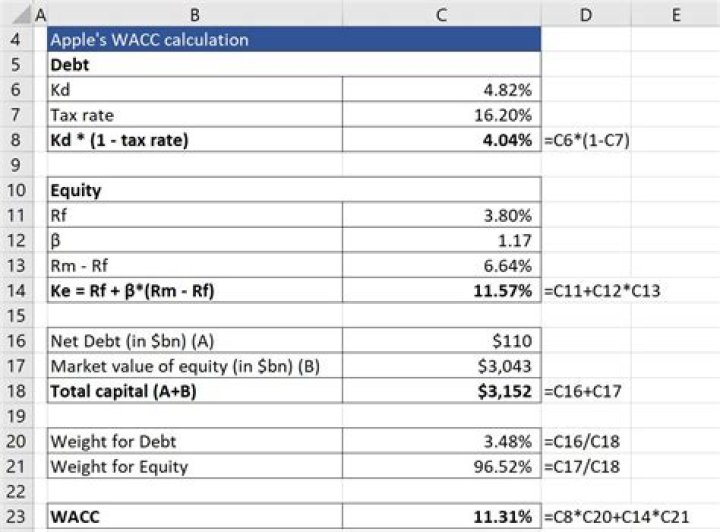

The formula is risk-free rate + beta * (market return – risk-free rate). The 10-year Treasury rate can be used as the risk-free rate and the expected market return is generally estimated to be 7%. Thus, Walmart’s cost of equity is 2.7% + 0.37 * (7% – 2.7%), or 4.3%.

Is a higher WACC better?

A high weighted average cost of capital, or WACC, is typically a signal of the higher risk associated with a firm’s operations. Investors tend to require an additional return to neutralize the additional risk. A company’s WACC can be used to estimate the expected costs for all of its financing.

Is it good to have high WACC?

Does WACC include depreciation?

Common expenses that are deductible include depreciation, amortization, mortgage payments and interest expense. This is not done for preferred stock because preferred dividends are paid with after-tax profits.

Is WACC real or nominal?

WACC must use nominal rates of return built up from real rates and expected inflation, because the expected UFCFs are expressed in nominal terms. WACC must be adjusted for the systematic risk borne by each provider of capital, since each expects a return that compensates for the risk assumed.

Which is the correct formula for calculating WACC?

WACC is calculated using the formula given below WACC = Weightage of Equity * Cost of Equity + Weightage of Debt * Cost of Debt * (1 – Tax Rate) WACC = 0.583 * 4.5% + 0.417 * 4.0% * (1 -32%) WACC = 3.76%

When was weighted average cost of capital ( WACC ) published?

This person is not on ResearchGate, or hasn’t claimed this research yet. This paper is a critical review on “The Weighted Average Cost of Capital (WACC) for Firm Valuation Calculations” by Fernando Llano-Ferro was published in International Research Journal of Finance and Economics, Issue 26 (2009).

What happens if the WACC rate is wrong?

If the WACC rate is wrong calculated, the result affects the firm value. It is essential of using methods to find the firm value without using of WACC rate and with it. The study by Rehman & Raoof (2010) examines Llano-Ferro’s (2009) approach by an example.

How is WACC calculated for equity based financing?

How to Calculate WACC. WACC is calculated by multiplying the cost of each capital source (debt and equity) by its relevant weight, and then adding the products together to determine the value. In the above formula, E/V represents the proportion of equity-based financing, while D/V represents the proportion of debt-based financing.