How do you close a general ledger account?

How to Close a General Ledger

- Debit the revenue account by the amount of its balance at the end of the accounting period to reduce it to zero.

- Credit each expense account by the amount of its balance to reduce each account’s balance to zero.

What is the journal entry to close sales?

The journal entries to close revenue accounts are to debit the revenue account and credit income summary, which is also a temporary account used for the closing process. The journal entries to close expense accounts are to credit the expense account and debit income summary.

What are the items that require adjusting entries?

5 Accounts That Need Adjusting Entries

- 1) Accrued Revenues. For any service performed in one month but billed in the next month would have adjusting entry showing the revenue in the month you performed the service.

- 2) Accrued Expenses.

- 3) Unearned Revenues.

- 4) Prepaid Expenses.

- 5) Depreciation.

What are permanent or real accounts?

Also referred to as real accounts. Accounts that do not close at the end of the accounting year. The permanent accounts are all of the balance sheet accounts (asset accounts, liability accounts, owner’s equity accounts) except for the owner’s drawing account.

Do you post closing entries to general ledger?

Before closing entries can be made, all transactions that took place before the end of the accounting period (which can be a month, quarter, or year) must be accounted for and posted to the general ledger. Posting closing entries, then, clears the way for financial statements to be made.

How do you record a closing entry?

Four Steps in Preparing Closing Entries

- Close all income accounts to Income Summary.

- Close all expense accounts to Income Summary.

- Close Income Summary to the appropriate capital account. Owner’s capital account for sole proprietorship.

- Close withdrawals/distributions to the appropriate capital account.

Where does inventory go in a general ledger?

The two accounts that are affected by the transaction are inventory and accounts payable. Go to the most recently used page in your inventory general ledger account. Inventory is an asset and asset increases are recorded in the debit column. A decrease in your inventory is recorded in the credit column.

What happens when you post journal entries to the general ledger?

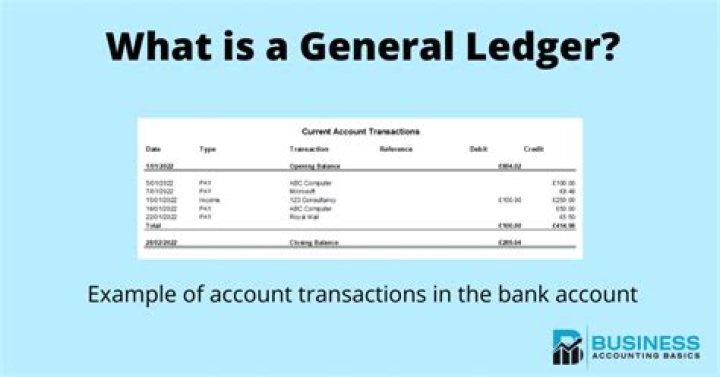

When posting journal entries to your general ledger, do not change any information. For example, if you debit an account in a journal entry, debit the same account in your ledger. Keep in mind that your general ledger lists all the transactions in a single account. This allows you to know the balance of each account.

How are subsidiary ledgers related to GL accounts?

In order to simplify the audit of accounting records or the analysis of records by internal stakeholders, subsidiary ledgers can be created. A subsidiary ledger (sub-ledger) is a sub-account related to a GL account that traces the transactions corresponding to a specific company, purchase, property, etc.

What are the different types of closing entries?

Closing Entries. Accounts are two different groups: Permanent – balance sheet accounts including assets, liabilities, and most equity accounts. These account balances roll over into the next period. So, the ending balance of this period will be the beginning balance for next period. Temporary – revenues, expenses,…