How long do you have to wait to refinance a house after bankruptcies?

Conventional mortgages: In most cases, you must wait four years from your bankruptcy discharge date before you can apply for conventional mortgage refinancing if you filed for Chapter 7 bankruptcy protection. Under extenuating circumstances, however, that waiting period may decrease to two years.

Can you refinance your mortgage if you are in Chapter 13?

A Chapter 13 bankruptcy does not disqualify you from refinancing a mortgage provided you made all your plan payments on time. Before refinancing, you must meet credit and income criteria and get the consent of the bankruptcy court.

Can you buy a house with a 590 credit score?

The most common type of loan available to borrowers with a 590 credit score is an FHA loan. FHA loans only require that you have a 500 credit score, so with a 590 FICO, you will definitely meet the credit score requirements. We can help match you with a mortgage lender that offers FHA loans in your location.

Depending on your loan type, Chapter 13 bankruptcies may allow refinance as early as a year into making payments (while you’re technically still in the bankruptcy period) or up to 2 years after discharge. You can refinance your home after a Chapter 7 bankruptcy between 2 – 4 years after discharge.

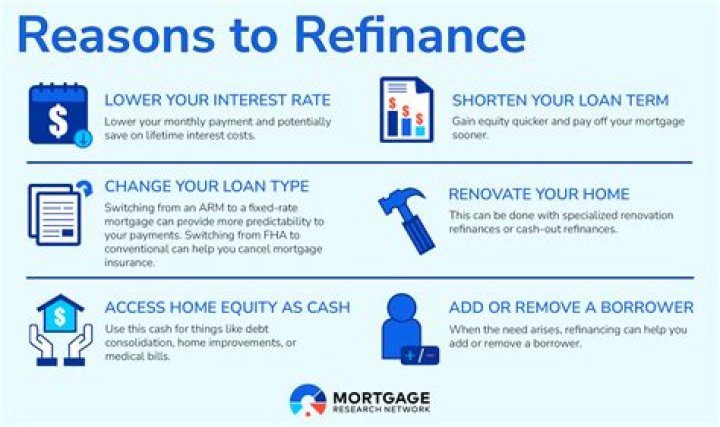

How soon can I refinance with owning?

You can refinance your mortgage as many times as it makes financial sense to do so. The only caveat is that you might have to wait six months from your most recent closing (whether it was a purchase or previous refinance) to do it again. Also, remember that refinancing includes closing costs.

Does owning only do refinancing?

Similar to CashCall’s No Closing Cost Mortgage, Owning will refinance your existing home loan with no closing costs, including third-party fees like appraisal, credit report, escrow, title insurance, and more.

When to refinance your home after Chapter 7 bankruptcy?

Depending on your loan type, Chapter 13 bankruptcies may allow refinance as early as a year into making payments (while you’re technically still in the bankruptcy period) or up to 2 years after discharge. You can refinance your home after a Chapter 7 bankruptcy between 2 – 4 years after discharge.

How long do you have to wait to refinance a VA loan?

Chapter 7: You must wait at least 2 years after the discharge or dismissal date before you can refinance your loan. The 2-year standard only applies to government-backed loans like FHA loans and VA loans. Most lenders require that you wait 4 years after your discharge date for a conventional loan. The waiting period on jumbo loans is 7 years.

How long does it take to refinance a FHA loan?

Federal Housing Administration loans: Government-backed loans, such as FHA loans, require that you wait at least two years from your Chapter 7 bankruptcy discharge date before refinancing. A discharge is a court order that prevents creditors from collecting qualifying debts.

How long do you have to wait to get a jumbo loan after bankruptcy?

Most lenders require that you wait 4 years after your discharge date for a conventional loan. The waiting period on jumbo loans is 7 years. Remember not to confuse your discharge date with the date you filed for bankruptcy.