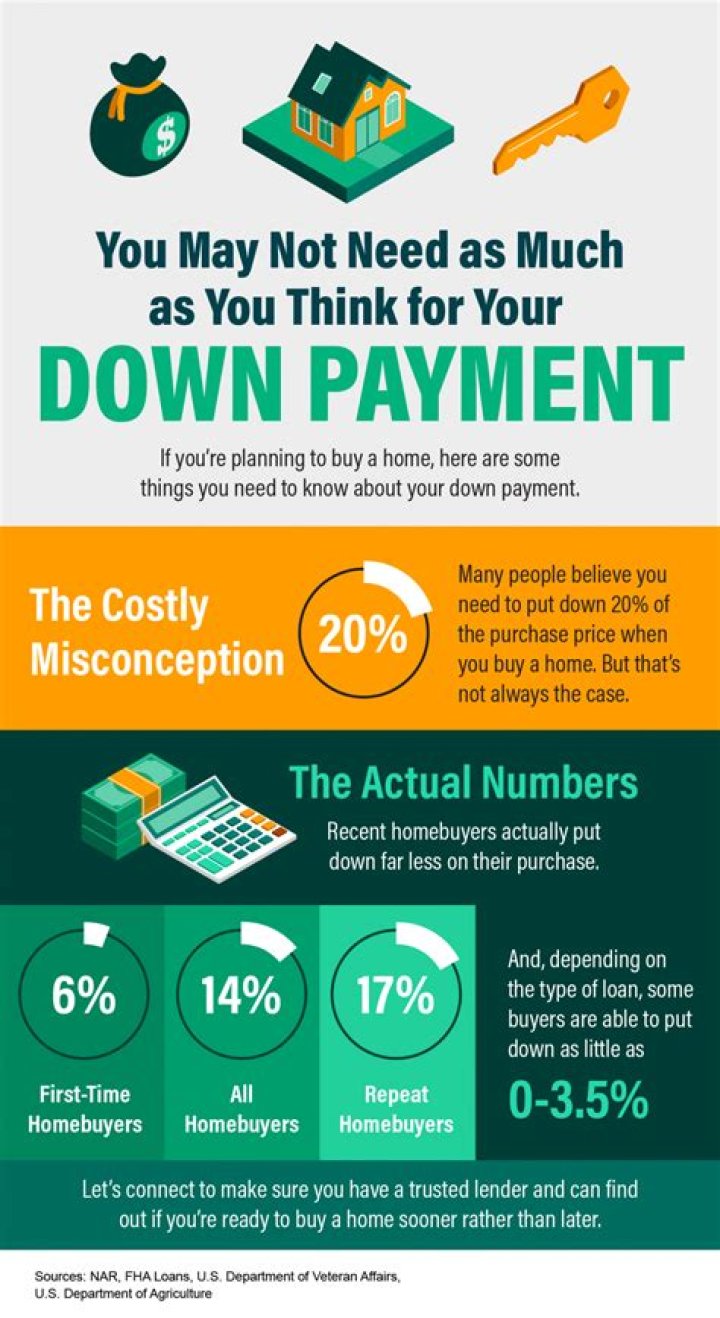

How much can be gifted for a down payment?

How much can be gifted for a down payment? As of 2018, parents can contribute a collective $30,000 per child to help with a down payment — anything after that would incur the gift tax. Other family members have a $15,000 lending limit before they, too, have to pay taxes.

Is a gift for a down payment taxable?

Is a gift for a down payment taxable? There may be tax implications when giving or receiving a cash down payment gift. The home buyer (person receiving the gift) typically shouldn’t have to pay taxes on the funds. The giver, however, may still have to pay taxes on the money they gifted.

Conventional loan You can use gifted money for the full down payment on a second home as well, so long as the cash gift equates to a 20% down payment or bigger. If the down payment on your second home is less than 20%, at least 5% must come from your own funds. Fannie Mae is a little stricter in this regard.

Can a seller give a buyer the down payment?

This is due to legal restrictions that prevent sellers from directly providing down payment assistance to home buyers. The seller gives the organization the necessary funds if the potential buyer secures the mortgage and closes on the home.

Can a gift of equity be used for a down payment on a home?

If you choose to put down 20% of the purchase price or more, it can all come from a gift. If you put down less than 20%, then only some of the money can be gifted. You’ll have to put down your own money and will have to be prepared to pay monthly mortgage insurance.

How much money can you get as a down payment gift?

How much money you’re eligible to receive as a down payment gift depends on the type of mortgage you’re borrowing. If you’re taking out a conventional loan – which means one that’s backed by Fannie Mae or Freddie Mac – all of your down payment can be gifted if you’re putting down 20% or more.

Can a down payment be a gift from Fannie Mae?

If you’re taking out a conventional mortgage through Freddie Mac or Fannie Mae, the entire down payment may be a gift if you put down 20 percent or more. In this case, you also have the added benefit of not having to pay private mortgage insurance. If you put down less than 20 percent, at least some of the money has to come from your funds.

Can you get a down payment gift for a second home?

In that scenario, you’d be responsible for paying at least 3.5% of the down payment yourself. Regardless of whether you’re getting a conventional, FHA or VA loan, a down payment gift is only acceptable when the house you’re purchasing will be your primary residence or second home.