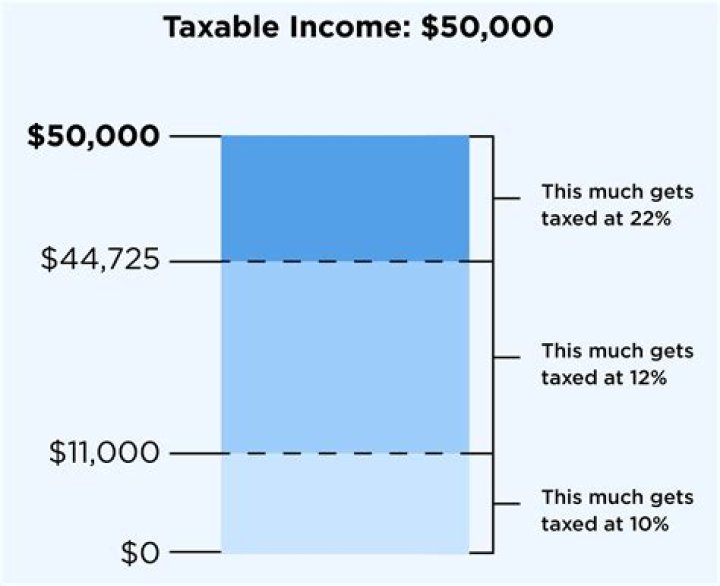

How much do you get taxed on buy to let income?

Yes. The income you receive as rent is taxable. You need to declare any rent you receive as part of your Self Assessment tax return. The tax on your income is then charged in accordance with your income tax banding (20% for basic rate taxpayers, 40% for higher rate, and 45% for additional rate).

Can I claim tax relief on buy to let?

Up to now, people buying to let have been able to claim tax relief on their mortgage interest payments at their marginal rate of tax. This means that a basic rate taxpayer would get 20 per cent tax relief, but those at a higher rate would receive 40 per cent relief, while top-rate taxpayers could claim 45 per cent.

What can I claim against tax for buy to let?

What HMRC rental property expenses are allowable on a buy to let property?

- Business rates or council tax;

- Rent paid to a superior landlord;

- Insurance;

- Management expenses;

- Advertising for tenants;

- Maintenance;

- Repairs such as:

- Repairing water leakages, gas leaks, burst pipes, electrical problems;

Is a washing machine tax deductible?

Charitable Deduction If you replace your existing HE washer and dryer with a new model, and donate your used appliances to a qualified charity, you can deduct the fair market value of the washer and dryer.

How long do I need to live in a property to avoid CGT?

You’re only liable to pay CGT on any property that isn’t your primary place of residence – i.e. your main home where you have lived for at least 2 years.

What are the tax rules for buy to let properties?

What are the tax rules for buy to let properties? Buy to let landlords used to be able to deduct 100% of the cost of financing their rental property (eg mortgages, loans and overdrafts) from their total rental income, eg if their rental income was £10,000 over the year and they repaid £10,000 of the mortgage, there would be no tax to pay.

What tax relief can you claim on buy-to-let in 2021?

From the tax relief you can claim on buy-to-let, to regulation changes outside of tax, here’s a run-down of what’s been announced – and what to watch out for this year. What is landlord insurance? 1. Tax relief on buy-to-let mortgages Not a new one exactly, but 2021 is the first full year where you can’t deduct mortgage expenses from rental income.

Are buy to let mortgages tax deductible?

Buy to let landlords used to be able to deduct 100% of the cost of financing their rental property (eg mortgages, loans and overdrafts) from their total rental income, eg if their rental income was £10,000 over the year and they repaid £10,000 of the mortgage, there would be no tax to pay. However, these tax rules were gradually changed.

What is buy-to-let mortgage interest tax relief and how does it work?

What is buy-to-let mortgage interest tax relief? Since April 2017, the way landlords have to declare their rental income has started to change, meaning most will see their tax bills rise significantly. While borrowing money through a buy-to-let mortgage was once a major tax advantage, it’s no longer the case.