Is Section 1231 property a capital asset?

Section 1231 does not reclassify property as a capital asset. Instead, it allows the taxpayer to treat net gains on 1231 property as capital gains, but to treat net losses on such property as ordinary losses.

Which of the following assets is 1231 property?

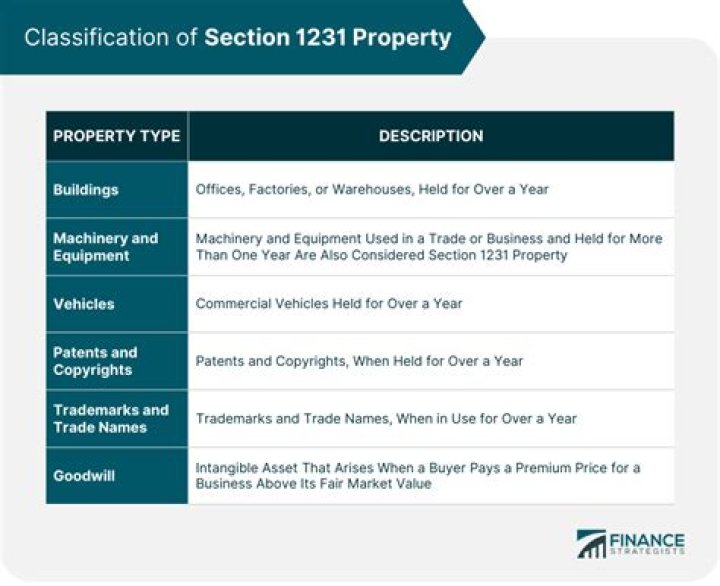

For a quick refresher, Section 1231 assets are defined as depreciable business property that has been held for more than a year. These assets can be buildings, machinery, land, timber and other natural resources, unharvested crops, cattle, livestock and leaseholds that are at least a year old.

What is capital asset property?

Capital assets are significant pieces of property such as homes, cars, investment properties, stocks, bonds, and even collectibles or art. For businesses, a capital asset is an asset with a useful life longer than a year that is not intended for sale in the regular course of the business’s operation.

Is rental property 1231 or 1250?

Commercial real estate, residential investment properties, buildings and land used for business are all section 1231 properties. Equipment, automobiles and furniture may also fall under section 1231, as can unharvested crops. Any piece of real estate that’s classified as a 1231 property is also a section 1250 property.

What type of property is 1250?

1250 Property is generally described as “real property,” and it has further been defined as “all depreciable property that is not 1245 property”.

Is real property a capital asset?

Real estate can indeed be a capital asset, but often it is classified as inventory, which by definition is not a capital asset. Any gain on inventory sales is business income, taxed at ordinary tax rates, not capital gain tax rates.

What is Section 1221 property?

Section 1221 defines “capital asset” as property held by the taxpayer, whether or not it is connected with the taxpayer’s trade or business. However, property used in a taxpayer=s trade or business and of a character that is subject to the allowance for depreciation provided in ‘ 167 is not a capital asset.

Is a Car 1231 property?

This may sound like semantics, but it’s important — a Section 1231 asset, as defined above, does not cease to be a Section 1231 asset because Sections 1245 or 1250 applies. The other depreciable properties (machinery, auto, furniture) are personal property, and as a result, are Section 1245 property.

What type of property is rental property 1250?

Section 1250 property – depreciable real property (like residential rental buildings), including leaseholds if they are subject to depreciation.

What are section 1231 assets?

The term “section 1231 property” or “1231 assets” is a tax term that refers to depreciable business property that has been held for over one year. The types of properties included in Section 1231 are machinery, land, cattle, timber, buildings, natural resources, crops, and leaseholds that are at least one year old.

Is goodwill a 1231 asset?

A capital asset is anything other than the things the tax law says it is not. Because goodwill is not on the list of non-capital assets, it is then a capital asset. Because your self-created goodwill was not amortizable by you, it is best classified as a capital asset rather than a Section 1231 asset.

Is goodwill a 1231 gain?

It includes such items as patents, copyrights, and the goodwill value of a business. Gain or loss on the sale or exchange of amortizable or depreciable intangible property held longer than 1 year (other than an amount recaptured as ordinary income) is a section 1231 gain or loss.

What is Section 1231, 1245, and 1250 property?

Put simply, section 1231 regulated the tax treatment of both gains and losses of depreciable property that’s been held for more than a year in a trade or business. Meanwhile, sections 1245 and 1250 include rules for recapturing depreciation applying to gains from dispositions .