What is a certification of non-foreign status?

With a Certification of Non-Foreign Status, the seller of real estate is certifying under penalty of perjury, that the seller is not foreign. The Affidavit is the form that is used by the seller to certify under Penalty of Perjury that the seller is not a foreign seller.

What is a non-foreign person?

A non-foreign person affidavit is made by a seller of a real property stating that s/he is a non-foreign seller as defined by the Internal Revenue Code Section 26 USC 1445. The non-foreign affidavit is required to afford the buyer with guarantee that the seller is not a foreign person.

What is a non-foreign certification by transferor?

Non-Foreign Certification – Transferee and Transferor. This form is provided so that the buyer and/or seller in this transaction can certify compliance with Foreign Investment in Real Property Tax Act to the escrow agent and/or buyer.

What is FIRPTA certificate?

FIRPTA Certificate: A FIRPTA certificate is used to to notify the IRS that the seller of real estate is not a foreign-person. The main FIRPTA form is the Foreign Investment in Real Property Act. The purpose of this law is to facilitate accurate withholding and compliance for U.S. tax purposes.

Who signs a FIRPTA certificate?

A: The buyer must agree to sign an affidavit stating that the purchase price is under $300,000 and the buyer intends to occupy. The buyer may choose not to sign the form, in which case withholding must be done.

Who delivers FIRPTA certificate?

BOSTON — Merger and acquisition agreements almost universally require the target or seller to deliver at closing a so-called “FIRPTA certificate” – i.e., an affidavit that either the target is not a “United States real property holding corporation” or that the seller is not a foreign person, in each case in accordance …

What is Certificate of Foreign Status?

Form W-8BEN2 is submitted by foreign individuals that receive income in the U.S. The form establishes that the person is a foreign individual and owner of said business. The W-8BEN is called the certificate of foreign status.

Who is considered a foreign person?

A foreign person includes a nonresident alien individual, foreign corporation, foreign partnership, foreign trust, foreign estate, and any other person that is not a U.S. person.

What is a foreign person for tax purposes?

A foreign person includes a nonresident alien individual, foreign corporation, foreign partnership, foreign trust, foreign estate, and any other person that is not a U.S. person. In most cases, the U.S. branch of a foreign corporation or partnership is treated as a foreign person.

Who provides a FIRPTA certificate?

Does FIRPTA apply to green card holders?

FIRPTA authorized the United States to tax foreign persons on dispositions of U.S. real property interests. Lawful permanent residents are often referred to as “green card” holders who are authorized by the federal government to live permanently within the United States as immigrants.

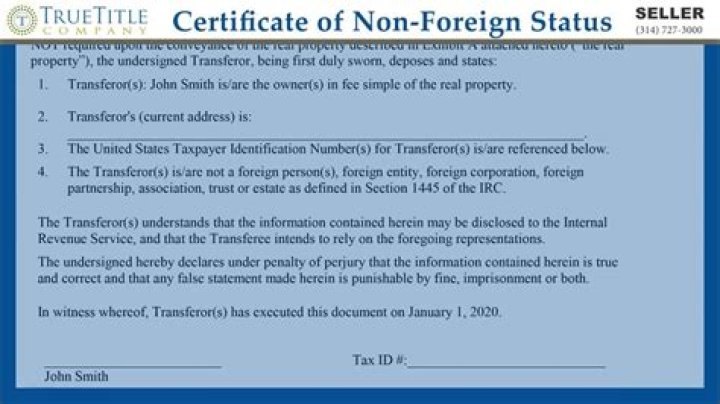

Seller’s certification of non-foreign status. A seller might be a U.S. resident for tax purposes by meeting the substantial presence test. In such cases, the seller can avoid having tax withheld by providing a certification of non-foreign status to the buyer. (A) States that the transferor is not a foreign person.

What is affidavit of non-foreign status section 1445?

AFFIDAVIT OF NON-FOREIGN STATUS Section 1445 of the Internal Revenue Code provides that a buyer of a United States real property interest must withhold tax if the seller is a foreign person.

Is [name of transferor] a foreign corporation?

[Name of transferor] is not a foreign corporation, foreign partnership, foreign trust, or foreign estate (as those terms are defined in the Internal Revenue Code and Income Tax Regulations); 2. [Name of transferor] is not a disregarded entity as defined in § 1.1445-2 (b) (2) (iii);

Is a transferor a non-resident alien for tax purposes?

2. The Transferor is not a non-resident alien for purposes of the U.S. income taxation (as such term is defined in the Internal Revenue Code and Income Tax Regulations). 3. The Transferor’s U.S. taxpayer identification number (Social Security Number) is