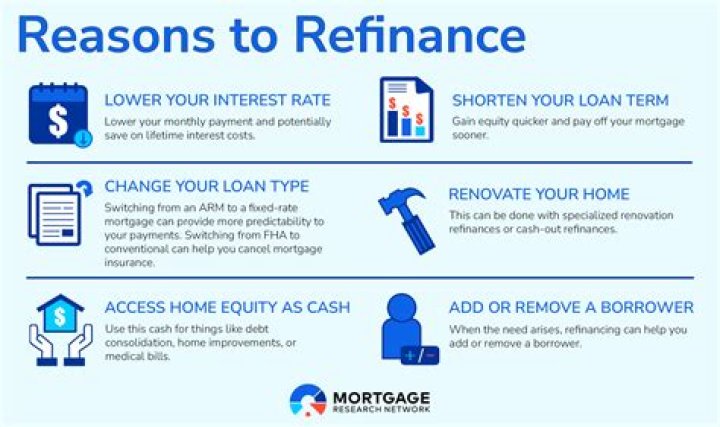

What is a common reason to refinance a first mortgage?

A common reason for homeowners to refinance is simply to lower their mortgage rate. If your current rate is higher than what’s being offered today, you should consider refinancing. You could lower your monthly mortgage payment, free up cash for other uses, or just make daily living a bit more comfortable.

Can you refinance just your first mortgage?

Refinancing only a first mortgage is possible if your home equity lender agrees to resubordination. This allows your refinanced mortgage to take the position before the old home equity loan.

How long do you have to have a mortgage to refinance?

You have to own and occupy the home as your principal residence for at least 12 months before applying for a cash-out refinance. You can do a cash-out refinance of a home you own free and clear. If you have a mortgage, you must have had it for at least six months.

Can you have 1 mortgage 2 houses?

Yes, one mortgage can cover two residential properties. In some cases, two houses stand on a single piece of land, with two separate addresses. If you are interested in financing a property like this, check your local bank or credit union and ask whether they work with portfolio loans.

What are the questions to ask when refinancing a mortgage?

First, ask each lender what types of loans they offer, the types of refinance options available and how to qualify for each. Then test your lender’s knowledge by asking about the difference between the interest rate and APR, how your monthly payment will change and what’s on your Closing Disclosure.

When is it a good time to refinance your mortgage?

If your mortgage has a higher interest rate compared to ones in the current market, then refinancing could be a smart financial move if it lowers your interest rate or shortens your payment schedule. If you can find a loan that offers a reduction of 1–2% in its interest rate, you should consider it.

What are the different types of refinancing mortgages?

There are different types of refinances. The two most common are: Rate-and-term refinances: Your mortgage rate is the percentage you pay in interest on your loan. Your mortgage term is the length of time you must make payments on your loan. As the name suggests, a rate-and-term refinance changes the rate and term of your mortgage loan.

Do You Pay Up Front for refinancing your mortgage?

But make no mistake; you pay for refinancing. One option, and the one recommended by most financial advisors, is to pay these costs upfront. Another is to roll them up into your loan, but it makes the loan amount higher and will take longer to break even.