What is a qualified withdrawal from an IRA?

You can withdraw Roth IRA contributions at any time, for any reason, without paying taxes or penalties. If you withdraw Roth IRA earnings before age 59½, a 10% penalty usually applies. Withdrawals before age 59½ from a traditional IRA trigger a 10% penalty tax, whether you withdraw contributions or earnings.

What are qualified education expenses for IRA withdrawal?

With funds from an IRA, a parent or student can pay for what are known as qualified education expenses – tuition, fees, books, supplies and equipment required for enrollment or attendance – without facing the penalty.

What is a qualified distribution from a Roth IRA?

A qualified distribution from your Roth IRA allows you to avoid taxes and the 10% early withdrawal penalty. To count as qualified, the distribution must meet both of these requirements: It occurs at least five years after you opened and funded your first Roth IRA (even if you’re withdrawing from a different one), and.

Can I withdraw from my IRA for education expenses?

Money in an IRA can be withdrawn early to pay for tuition and other qualified higher education expenses for you, your spouse, children, or grandchildren—without penalty. To avoid paying a 10% early withdrawal penalty, the IRS requires proof that the student is attending an eligible institution.

The term qualified distribution refers to a withdrawal from a qualified retirement plan. These distributions are both tax- and penalty-free. Eligible plans from which a qualified distribution can be made include 401(k)s and 403(b)s. Qualified distributions can’t be used at an investor’s discretion.

What are qualified medical expenses for IRA withdrawal?

Generally speaking, you can take an IRA hardship withdrawal to cover the following expenses: Unreimbursed medical expenses that exceed more than 7.5% of adjusted gross income (AGI) or 10% if younger than 65. Qualified higher education expenses. Purchasing your first-home that doesn’t exceed $10,000.

Can IRA funds be withdrawn without penalty?

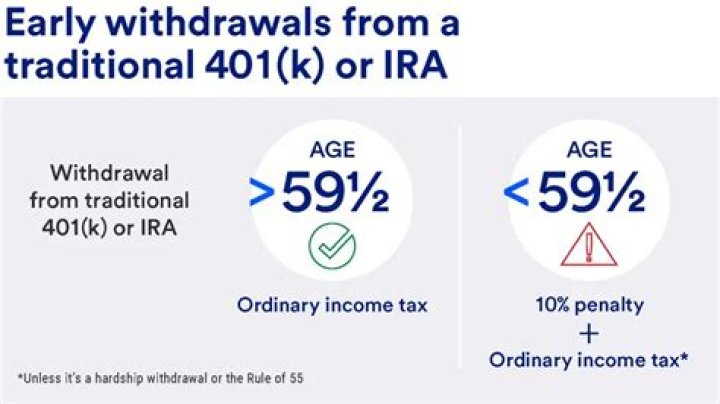

Once you reach age 59½, you can withdraw funds from your Traditional IRA without restrictions or penalties.

What are qualified distributions?

Tax-deferred plans include traditional IRAs, simplified employee pension IRAs, savings incentive match plans for employees IRAs, traditional 401(k)s and traditional 403(b)s. When you take a qualified distribution from a tax-deferred plan, you still owe income taxes, but you won’t pay any early withdrawal penalties.

Will I get penalized for taking money out of my IRA?

Generally, early withdrawal from an Individual Retirement Account (IRA) prior to age 59½ is subject to being included in gross income plus a 10 percent additional tax penalty. There are exceptions to the 10 percent penalty, such as using IRA funds to pay your medical insurance premium after a job loss.

What are the rules for withdrawals from an IRA?

There are several rules for withdrawals that apply before you reach retirement age, and others for when you’re ready to retire and enjoy the fruits of your labors. There are five main types of IRA withdrawals: early, regular withdrawals, Required Minimum Distributions (RMDs), Roth IRA withdrawals, and IRA rollovers or transfers.

What can be covered by a hardship withdrawal from an IRA?

Generally speaking, you can take an IRA hardship withdrawal to cover the following expenses: Unreimbursed medical expenses that exceed more than 7.5% of adjusted gross income (AGI) or 10% if younger than 65. Qualified higher education expenses. Purchasing your first-home that doesn’t exceed $10,000.

Can you withdraw money from an IRA without penalty?

Under normal circumstances, you cannot withdraw money from your traditional individual retirement account (IRA) without facing a penalty tax until you reach age 59.5. You can, however, avoid this sanction if you make an IRA hardship withdrawal.

Do you have to report an IRA withdrawal to the IRS?

You may be able to avoid the penalty tax portion if your situation falls under the IRA withdrawal hardship rules. Don’t forget to report the withdrawal because the custodian of the IRA will report it to the IRS. You will owe taxes and penalties once they notice that you didn’t claim the income.