What is deferred tax expense?

Deferred tax expense. A non-cash expense that provides a source of free cash flow. Amount allocated during the period to cover tax liabilities that have not yet been paid.

Is Amlp tax efficient?

AMLP’s effective tax rate is significantly lower than that of KYN, probably due to the fund’s lower turnover, it is an index fund after all, and lower shareholder returns. Moving forward, tax expenses are almost certainly going to be significantly lower, if not zero, due to the fund’s significant past losses.

What is Alerian MLP etf?

About Alerian MLP ETF The underlying index is comprised of energy infrastructure MLPs that earn a majority of their cash flow from the transportation, storage and processing of energy commodities. It is non-diversified.

How do you calculate deferred income tax expense?

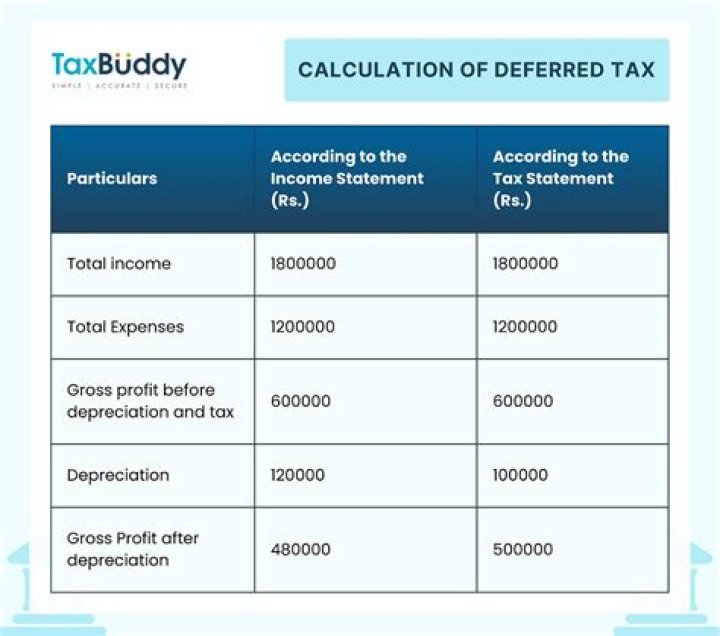

In that post, we recalled the basic formula determining the income tax provision: Current tax expense/benefit + Deferred tax expense/benefit = Total income tax expense or benefit as reported in the financial statements.

What is an example of a deferred expense?

Common examples of deferred expenditures include: Advertising fees. Advance payment of insurance coverage. An intangible asset cost that is deferred due to amortisation. Tangible asset depreciation costs.

Does AMLP use leverage?

In the case of AMLP, the fund’s market value is based on 100% daily leverage while the fund’s NAV calculation (what the shareholder sees) uses 62.5% leverage and seeks to track 62.5% of the daily change of the underlying index.

What happens when you sell AMLP?

When an MLP is sold, all loss carryovers for that particular MLP become deductible that year. At that time, those losses can be used to offset other income, including ordinary or capital gain income and income from other MLPs.

Is AMLP a k1 or 1099?

AMLP is the largest MLP product, providing access to midstream energy infrastructure MLPs with a 1099 tax form and no K-1s.

What is the journal entry for deferred income?

You need to make a deferred revenue journal entry. When you receive the money, you will debit it to your cash account because the amount of cash your business has increased. And, you will credit your deferred revenue account because the amount of deferred revenue is increasing.

How do you record deferred expenses?

Accounting for Deferred Expenses Like deferred revenues, deferred expenses are not reported on the income statement. Instead, they are recorded as an asset on the balance sheet until the expenses are incurred. As the expenses are incurred the asset is decreased and the expense is recorded on the income statement.

What is the deferred tax liability at the end of life?

At the end of the life of the asset, no deferred tax liability exists, as the total depreciation between the two methods is equal. A deferred income tax liability results from the difference between the income tax expense reported on the income statement and the income tax payable, which is on the balance sheet.

How is deferred income tax liability calculated under GAAP?

GAAP accounting requires the calculation and disclosure of economic events in a specific manner. Income tax expense, which is a financial accounting record, is calculated using GAAP income. A deferred income tax liability results from the difference between the income tax expense reported on the income statement and the income tax payable.

What are the deferred income tax variations?

Deferred Income Tax Variations. A deferred income tax liability results from the difference between the income tax expense reported on the income statement and the income tax payable, which is on the balance sheet. A deferred income tax liability is classified on a balance sheet. It may be classified as either a short-term or current,…

How is deferred income tax liability classified on a balance sheet?

A deferred income tax liability is classified on a balance sheet. It may be classified as either a short-term or current, liability or as a long-term liability. If the deferred tax liability is presumed to be paid in the next 12 months, it must be recorded as a current liability.