What is lag in VAR model?

A lag is the value of a variable in a previous time period. So in general a pth-order VAR refers to a VAR model which includes lags for the last p time periods.

How do I choose lag length in VAR?

1 Answer. In general lag length in VAR models is selected using statistical information criteria. This means that VAR models are fitted for various lengths an certain statistic is calculated. The lag length is taken to be of model with the smallest statistic.

What are the different lag criterions we study under VAR analysis?

The six criteria are the Schwarz Information Criterion (SIC), the Hannan-Quinn Criterion (HQC), the Akaike Information Criterion (AIC), the general-to-specific sequential Likelihood Ratio test (LR), a small-sample correction to that test (SLR) proposed by Sims (1980), and the specific-to-general sequential Portmanteau …

When should I apply VAR?

Vector Autoregression (VAR) is a multivariate forecasting algorithm that is used when two or more time series influence each other. That means, the basic requirements in order to use VAR are: You need at least two time series (variables) The time series should influence each other.

What is the difference between VAR and Arima?

On the other hand, VAR can be estimated using OLS or GLS which are generally fast, while ARIMAX requires maximum likelihood estimation which is generally slow. Whether VAR or ARIMAX provides a better representation of the underlying process in your application is an empirical question.

How many lags should I use?

Also, from Jeffery Wooldridge’s Introductory Econometrics: A Modern Approach with annual data, the number of lags is typically small, 1 or 2 lags in order not to lose degrees of freedom. With quarterly data, 1 to 8 lags is appropriate, and for monthly data, 6, 12 or 24 lags can be used given sufficient data points.

When should we use VAR model?

Why do we use VAR model?

The VAR model has proven to be especially useful for describing the dynamic behavior of economic and financial time series and for forecasting. It often provides superior forecasts to those from univari- ate time series models and elaborate theory-based simultaneous equations models.

What is lag order?

A lag plot is a special type of scatter plot with the two variables (X,Y) “lagged.” A “lag” is a fixed amount of passing time; One set of observations in a time series is plotted (lagged) against a second, later set of data. The most commonly used lag is 1, called a first-order lag plot.

What is vector autoregressive model in time series?

The vector autoregressive (VAR) model is a workhouse multivariate time series model that relates current observations of a variable with past observations of itself and past observations of other variables in the system. Ability to capture the intertwined dynamics of time series data.

How does var select work with lag?

Second, the function VARselectconsiders only unrestricted models. By that I mean, if lag $k$ is included, lag $k-1$ will also be included; the function does not consider, for example, VAR(12) where all lag 1 through lag 11 coefficients are restricted to zero. Meanwhile, a relevant model for your data could perhaps be VAR(3) plus the 12th lag.

How do you find the standard errors of lag 1 variables?

The first row gives the standard errors of the coefficients for the lag 1 variables that predict y1. The second row gives the standard errors for the coefficients that predict y2. You may note that the coefficients are close to the VAR command except the intercept.

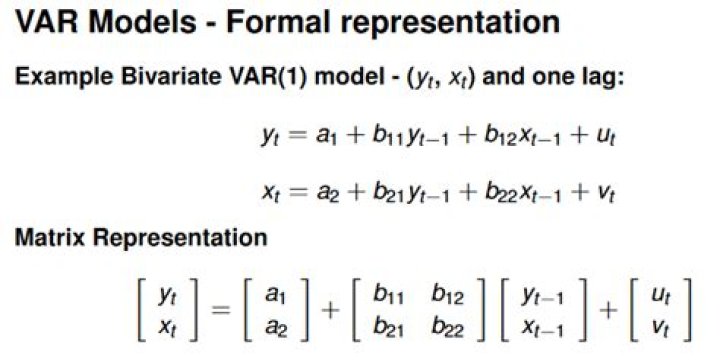

What is a Var(1) model?

The above equation is referred to as a VAR (1) model, because, each equation is of order 1, that is, it contains up to one lag of each of the predictors (Y1 and Y2). Since the Y terms in the equations are interrelated, the Y’s are considered as endogenous variables, rather than as exogenous predictors.

Why is var considered as an autoregressive model?

It is considered as an Autoregressive model because, each variable (Time Series) is modeled as a function of the past values, that is the predictors are nothing but the lags (time delayed value) of the series. Ok, so how is VAR different from other Autoregressive models like AR, ARMA or ARIMA?