What is loss allowed by basis limitation?

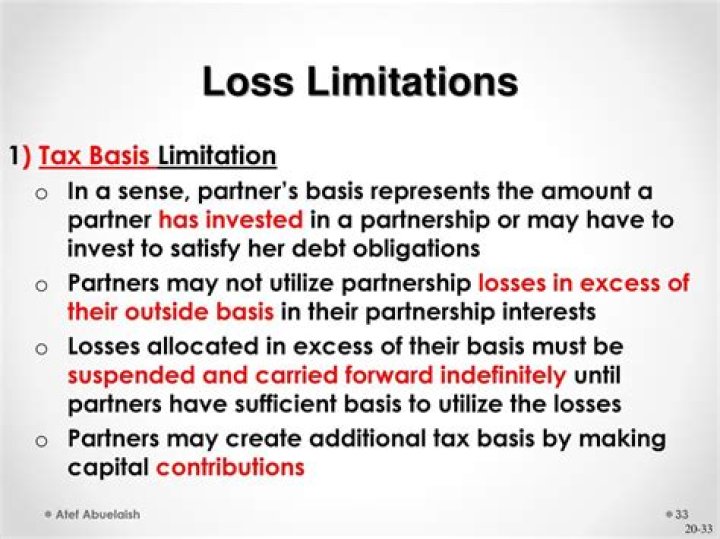

The first of these limitations is the basis limitation , which limits the losses and deductions to the adjusted basis in the activity at year-end. Any amount of loss and deduction in excess of the adjusted basis at the end of the year is disallowed in the current year and carried forward indefinitely.

What are potential limitations on partnership losses?

If, in a given taxable year, a partner’s share of partnership losses exceeds its outside basis, then the losses are allowed to the extent of basis and any excess amount is carried over for use in the next taxable year in which the partner has outside basis available.

What does PYA basis limitation mean?

Definition. The basis limitation is a limitation on the amount of losses and deductions that a partner of a partnership or a shareholder of an S-Corporation can deduct. Per Schedule E (1040), shareholders of S-Corporations are required to attach a basis calculation to their tax return each year.

What is the order of loss limitation rules?

Loss Ordering – Three Limitations Ordering rule: first determine if there is sufficient basis, then whether the taxpayer is at-risk, and finally whether the losses are passive. If there is insufficient basis to absorb losses, then the other two limitations need not be considered.

Does at risk basis include recourse debt?

At-risk basis is the cumulative result of a taxpayer’s (1) contributions and distributions of cash and the adjusted basis of property contributed; (2) borrowings to the extent the taxpayer is liable for repayment or has pledged property, other than property used in the activity, as security for the borrowed amounts ( …

What is the adjusted basis of property?

Adjusted basis refers to how much you lose or gain when you sell property. Before you can determine your profit or loss from the sale or exchange of property, you must factor in things such as depreciation or money you invested in improvements to the property prior to selling it.

The basis limitation is a limitation on the amount of losses and deductions that a partner of a partnership or a shareholder of an S-Corporation can deduct.

What are the four limitations on potential losses?

Taxpayers need to go through the four types of limitation hurdles before being able to deduct their losses: basis limitations, at-risk limitations, passive loss rules, and the new excess business loss limitations.

What is the difference between basis limitation and at risk limitation?

The amount you have at-risk is similar to basis in that you cannot deduct losses in excess of your at risk amount. The amount at-risk, however, is not the same as basis. In many cases, a taxpayer can still have basis, but his losses are not deductible because they are limited by the amount at risk.

Can General Partners deduct losses?

Losses suspended under the at-risk rules may become deductible in a year in which a partner does not have tax basis in his partnership interest. The deduction of the suspended losses in a subsequent year reduces the amount the taxpayer is at risk (Sec. 465(b)(5)).

When is section 382 limitation on net operating loss increased?

the long-term tax -exempt rate. If the section 382 limitation for any post-change year exceeds the taxable income of the new loss corporation for such year which was offset by pre-change losses, the section 382 limitation for the next post-change year shall be increased by the amount of such excess.

What is the carryforward of the section 382 limitation?

(2) Carryforward of unused limitation. If the section 382 limitation for any post-change year exceeds the taxable income of the new loss corporation for such year which was offset by pre-change losses, the section 382 limitation for the next post-change year shall be increased by the amount of such excess.

When is the limitation on net operating loss zero?

Except as provided in paragraph (2), if the new loss corporation does not continue the business enterprise of the old loss corporation at all times during the 2-year period beginning on the change date, the section 382 limitation for any post-change year shall be zero.

What are the rules for limitation under section 383?

Similar rules shall apply in the case of any credit or loss subject to limitation under section 383. taxable income shall be treated as having been offset first by the loss subject to such limitation. in the case of attribution from another entity, an interest in such entity similar to stock described in subclause (I).