What is Murabaha profit?

Murabaha is an Islamic financing structure that works as a sales contract, fixing the price of goods or items as required by a customer, inclusive of a pre-agreed profit margin. The customer repays the bank according to pre-defined installments or settlement terms.

How is Murabaha loan calculated?

Profit= [Amount Financed (F) * Profit Rate(R) * Term of financing] Profit= [1,000,000*5%*60/12] = 250,000. In case of an early payment, the customer may get a rebate.

How does Islamic banking earn profit?

Answer: The Islamic bank uses its funds in various trade, investment and service related Shariah compliant activities and earns profit thereupon. The profit earned from such activities is passed on to the depositors according to the agreed terms.

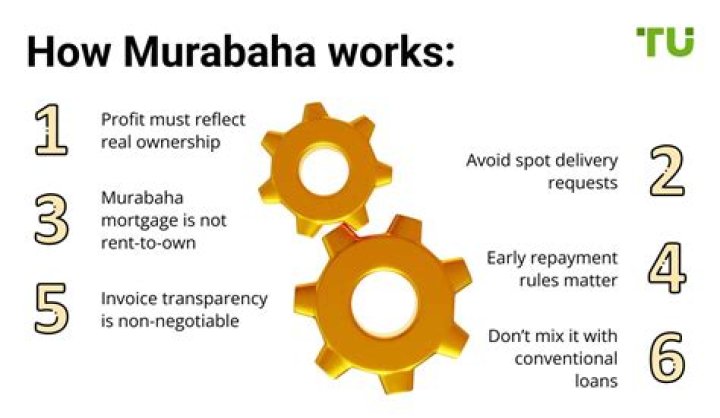

What are the basic rules for Murabaha financing?

Murabaha (cost plus trade financing)

- the subject of the transaction must exist at the time of the sale and be identified to the buyer;

- the seller must possess the subject matter at the time of sale and the sale must be instant, absolute and unconditional;

- the subject matter should be a property having value;

How does a murabaha work?

In a murabaha transaction, a financing party buys an asset that has been identified by its client (borrower) from a third-party and then sells that asset to the borrower for the original purchase price plus a profit element (generally calculated based on a benchmark figure such as LIBOR). …

How banks earn their profit through Murabahah?

In a murabaha contract of sale, a client petitions a bank to purchase an item on their behalf. In a murabaha contract for sale, the bank buys an asset and then sells the asset back to the client with a profit charge. This type of transaction is halal or valid, according to Islamic Sharia/Sharīʿah.

What is Murabaha used for?

Murabaha is a commonly known Working Capital Finance widely used in Islamic Banks. Murabaha refers to sale where the seller discloses the cost of commodity and the amount of profit charged. Thus it is not a loan given on interest rather it is a sale of commodity at profit.

What is Gharar in Islamic banking?

The word gharar means uncertainty, hazards, or risk. In Islamic finance, gharar is prohibited because it runs counter to the notion of certainty and openness in business dealings. Gharar can arise when the claim of ownership is unclear or suspicious.

What is Murabaha financing?

Murabaha: (Cost-plus financing) This is a contract sale between the bank and its client for the sale of goods at a price which includes a profit margin agreed by both parties. As a financing technique, it involves the purchase of goods by the bank as requested by its client. The goods are sold to the client with a mark-up.

How is the Murabahah price determined?

The murabahah price can be determined on the basis of the market rate of dollars on the date when the bank has paid the price to the supplier. (b) The bank determines the murabahah price in US dollars rather than in Pak rupees, so that the deferred murabahah price is paid by the customer in dollars.

What is murabaha (mark up)?

Murabaha is the most popular and most common mode of Islamic inancing. It is also known as Mark up or Cost plus financing. The word Murabaha is derived from the Arabic word Ribh that means profit. Originally, Murabaha was a contract of sale in which a ommodity is sold on profit.

What are the requirements of murabaha sale?

Another important requirement of Murabaha sale is that two sale contracts, one through which the bank acquires the commodity and the other through which it sells it to the client should be separate and real transactions. The Murabaha form of financing is being widely used by the Islamic banks to satisfy various kinds of financing requirements.