What is non-commercial loss rule?

The non-commercial loss rules determine whether the loss, or your share of the loss, is deductible in the current year. Your net small business income, or share of net small business income, is only reduced by losses deductible in the current year.

Can you choose to defer non-commercial losses?

If you don’t meet any of the non-commercial business loss requirements, you can defer the loss or carry it forward to future years. See also: Non-commercial losses – work out if you offset or defer the loss. Losses – including what is a tax loss and how to claim a tax loss.

What is a non-commercial business activity?

A “non-commercial” business activity in this context is any business where the deductions exceed the assessable income in any particular year. the total value of real property (or interests in real property) used on a continuing basis to carry out the business is at least $500,000; or.

What is deferred non-commercial business losses?

The deferred loss is a deduction when calculating any net profit or loss from the activity in that future year. Your deferred loss deduction may be reduced if: you earn net exempt income in the future year, or.

What is non-commercial income?

Non-commercial means something is not primarily intended for, or directed towards, commercial advantage or monetary compensation by an individual or organisation. Your use of someone else’s work should not conflict with the legitimate interests of the creator of an artistic work.

What does it mean to defer a loss?

The deferred loss is a deduction when calculating any net profit or loss from the activity in that future year.

Can you choose to defer a loss?

If you cannot offset your losses, deferring losses as a sole trader is possible. However, each situation is different, and this is assessed on a case by case basis. There are a number of requirements you must satisfy if you wish to defer losses as a sole trader.

How do you defer a business loss?

If you can’t deduct your business activity loss in the current year, you can defer your loss for use in a later year. If your business makes a profit in a following year, you can offset some or all of the deferred loss against this profit, up to the amount of your profit.

What is assessable income for non-commercial losses?

To meet the income requirement the taxpayer’s income must be less than $250,000. The income is calculated as the taxable income (ignoring any business losses), total reportable fringe benefits amounts, reportable superannuation contributions, and total net investment losses.

What are non-commercial purposes?

Non-commercial use encompasses a wide range of exciting possibilities—including artistic, educational, scholarly, and personal projects that will not be marketed, promoted, or sold.

What is considered non-commercial use?

What is the difference between commercial use and personal use?

Personal use is not to be used for profit or commercial gain. These projects usually have a very limited audience, say, for a personal party invite. Whereas commercial or for-profit use is intended for promotional, marketing or advertising a service, person or business.

What are non-commercial products?

non-commercial goods means goods that are intended for the personal or family use of the consignee or persons carrying them, or which are clearly intended as gifts and the aggregate value or quantity of which does not exceed the amounts laid down in directives issued by the Ministry; Sample 1. Save.

Is government considered non-commercial?

Governmental organizations are not regarded as non-commercial and will require a license to be in line with our terms and conditions.

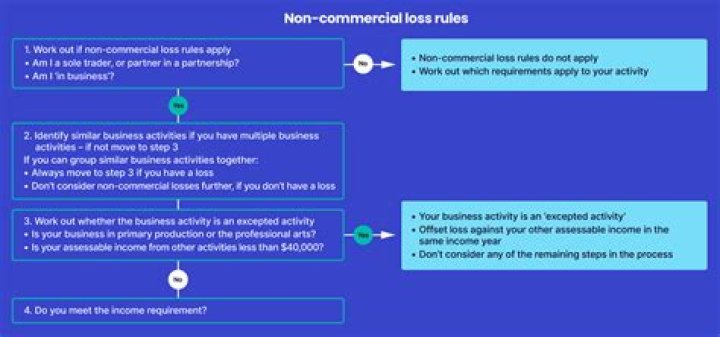

Any losses you incur as a sole trader or partnership in business are called “Non-commercial Losses”. If the tests are passed, individual taxpayers can benefit from these losses by offsetting them against other income such as salary and wages, providing an effective way to minimise their taxable income.

Do you have to apply non-commercial losses?

If you’re a primary producer or a professional artist and your income from other sources that do not relate to the business is less than $40,000 (excluding net capital gains), the non-commercial loss rules will not apply to you.

You can’t claim a loss for a business that is little more than a hobby or lifestyle choice. In this case, you can defer the loss until you make a profit from the business. …

What are deferred non-commercial business losses?

What is the difference between commercial and non-commercial?

Non-commercial use encompasses a wide range of exciting possibilities—including artistic, educational, scholarly, and personal projects that will not be marketed, promoted, or sold. Commercial use is any reproduction or purpose that is marketed, promoted, or sold and incorporates a financial transaction.

Can you choose to defer a business loss?

You can technically defer your losses indefinitely whilst ever you have a similar framework. However, this will cease when any one of the following applies: There is a profit from your business activity, in which case the deferred loss can be offset to the extent of the profit from the business activity.

How long can you defer business losses?

Business Loss Deduction Limit If you’ve only been in business two years and you’ve shown a loss in both, you can file Form 5213 to defer an IRS decision until five years have passed.

Can you deduct losses from a non-passive LLC?

The good news is you can avoid the PAL rules if you materially participate in the loss-generating activity. In other words, meeting the material participation standard makes the activity non-passive, which means you can deduct the losses currently, assuming no other tax-law provision prevents you from doing so.

How does clearinghouse work for commercial drivers license?

Employers will be required to query the Clearinghouse for current and prospective employees’ drug and alcohol violations before permitting those employees to operate a commercial motor vehicle (CMV) on public roads. Employers will be required to annually query the Clearinghouse for each driver they currently employ.

Can a LLC be used as a passivelosse?

With some very specific exceptions, rental losses, from LLCs or otherwise, are passivelosses by definition.) Using an LLC to own and operate a business shields your personal assets from most business-related liabilities. This liability protection advantage is similar to what you get with a corporation.

Which is the easiest way to deduct losses?

The following two tests are by far the easiest. * Substantially-All Test: You pass if your participation (time spent) in the loss-generating activity during the year in question constitutes substantially all participation by all individuals. Basically, if you do all the work, you pass this test even if it doesn’t take much time.