What is qualified IRA?

A qualified retirement plan is an investment plan offered by an employer that qualifies for tax breaks under the Internal Revenue Service (IRS) and ERISA guidelines. An individual retirement account (IRA) is not offered (with the exception of SEP IRAs and SIMPLE IRAs) by an employer.

What is qualified vs non-qualified?

Qualified retirement plans give employers a tax break for any contributions they make. Employees also get to put pre-tax money into a qualified retirement plan. All workers must get the same opportunity to benefit. A non-qualified plan has its own rules for contributions, but offers the employer no tax break.

What makes a qualified retirement plan qualified?

A qualified retirement plan is a retirement plan recognized by the IRS where investment income accumulates tax-deferred. Common examples include individual retirement accounts (IRAs), pension plans and Keogh plans. Most retirement plans offered through your job are qualified plans.

What is considered qualified money?

Qualified money basically refers to money in retirement accounts, such as IRAs, 401(k)s, and 403(b)s. ERISA, or the Employee Retirement Income Security Act, invented qualified money. Before 1974, the only retirement accounts that existed were really just pensions.

What is qualified vs non-qualified tax status?

Qualified plans have tax-deferred contributions from the employee, and employers may deduct amounts they contribute to the plan. Nonqualified plans use after-tax dollars to fund them, and in most cases employers cannot claim their contributions as a tax deduction.

What are examples of qualified accounts?

Some examples:

- Qualified plans include 401(k) plans, 403(b) plans, profit-sharing plans, and Keogh (HR-10) plans.

- Nonqualified plans include deferred-compensation plans, executive bonus plans, and split-dollar life insurance plans.

How are non-qualified distributions taxed?

Earnings distributed from non-qualified education savings plans are taxable and may be subject to a 10% IRS early withdrawal penalty. Non-qualified Roth distributions are taxed as income and may be subject to the IRS premature withdrawal penalty.

How is a non-qualified pension taxed?

Contributions to a nonqualified plan will lower your current income taxes (you must still pay Social Security and Medicare taxes). You will owe taxes when you receive your plan payouts so it provides a way to manage the timing of your tax payments prior to retirement.

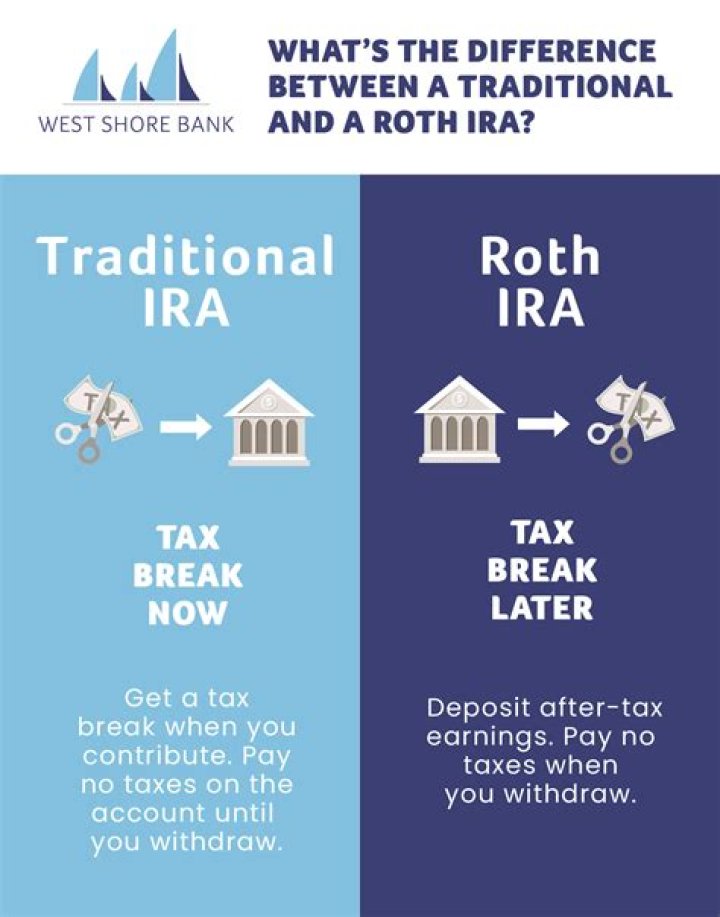

What is considered a qualified Roth IRA distribution?

Any earnings you withdraw are considered “qualified distributions” if you’re 59½ or older, and the account is at least five years old, making them tax- and penalty-free. Other kinds of withdrawals are considered “non-qualified” and can result in both taxes and penalties.

What are the two characteristics of a qualified retirement plan?

Qualified plans have the following features: employer’s contributions are tax-deductible as a business expense; employee contributions are made with pretax dollars contributions are not taxed until withdrawn; and interest earned on contributions is tax-deferred until withdrawn upon retirement.

What is considered a non qualified retirement plan?

A nonqualified plan is a type of tax-deferred, employer-sponsored retirement plan that falls outside of Employee Retirement Income Security Act (ERISA) guidelines. These plans are also exempt from the discriminatory and top-heavy testing that qualified plans are subject to.