What is recoverable amount impairment?

An asset is impaired when its carrying amount exceeds the recoverable amount. The recoverable amount is, in turn, defined as the higher of the fair value less cost to sell and the value in use; where the value in use is the present value of the future cash flows. An impairment review calculation looks like this.

How do you calculate impairment loss?

Impairments take the difference between the book value and fair market value and report the difference as an impairment loss.

- Subtract the fair market value of the asset from the book value of the asset.

- Determine if you are going to hold on and use the asset or if you are going to dispose of the asset.

How do you calculate depreciation after impairment loss?

Using straight-line depreciation, calculate the annual depreciation by dividing the original cost by the number of years in useful life. In this example, the equipment cost $2 million and had an estimated useful life of 10 years. Use the equation $2 million / 10 = $200,000. This is the annual depreciation amount.

What is the recoverable amount of an asset?

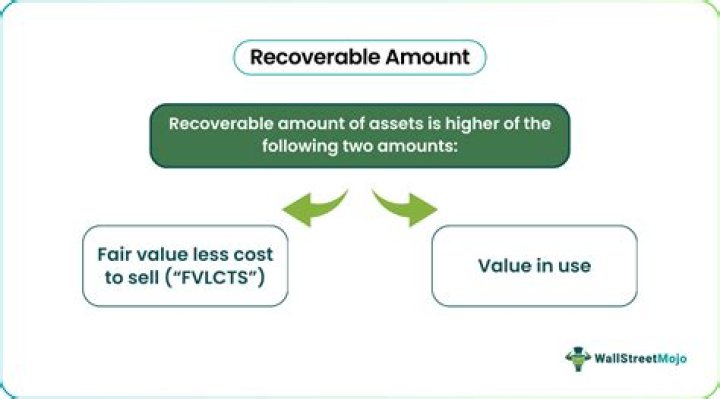

The recoverable amount of an asset refers to the present value of the expected cash flows that are to arise from the sale or use of the asset and is calculated as greater of the two amounts, namely, the fair value of the asset as reduced by the related selling costs, and value in the use of such assets.

How is recoverable amount calculated?

It is calculated by finding out probability-weighted future cash flows of the asset (or the cash-generating unit containing the asset, if no cash flows can be identified for the asset itself) and discounting those cash flows using a discount rate that reflects the risk of the cash flows.

How do you calculate recoverable amount?

How do you calculate recoverable assets?

How to Determine an Asset’s Recoverable Amount. An asset’s recoverable amount is the higher dollar amount of its fair value less cost to sell or its value in use. The cost to sell is exactly what it sounds like — the amount it costs you to sell the asset.

How do you determine recoverable amount?

How does impairment loss affect balance sheet?

Impairment exists when an asset’s fair value is less than its carrying value on the balance sheet. An impairment loss records an expense in the current period which appears on the income statement and simultaneously reduces the value of the impaired asset on the balance sheet.

Is impairment loss tax deductible?

Any impairment loss or any provisions, including provision for impairment loss would not be deductible for tax purposes. 5.1. For such companies, impairment losses may be allowed for tax deduction where the valuation amount is within the meaning allowed under Section 35(3) of the Income Tax Act, 1967.

Is recoverable amount fair value?

Recoverable amount is the greater of an asset’s fair value less costs to sell, or its value in use. Thus, the concept essentially focuses on the greatest value that can be obtained from an asset, either by selling or using it.

Is impairment loss a non-cash expense?

A non-cash charge is a write-down or accounting expense that does not involve a cash payment. Depreciation, amortization, depletion, stock-based compensation, and asset impairments are common non-cash charges that reduce earnings but not cash flows.

Is an impairment loss an expense?

An impairment loss records an expense in the current period which appears on the income statement and simultaneously reduces the value of the impaired asset on the balance sheet.

How do you treat impairment loss?

Recognition of an impairment loss

- An impairment loss is recognised whenever recoverable amount is below carrying amount. [

- The impairment loss is recognised as an expense (unless it relates to a revalued asset where the impairment loss is treated as a revaluation decrease). [

- Adjust depreciation for future periods. [

What is the journal entry for impairment loss?

The total dollar value of an impairment is the difference between the asset’s carrying cost and the lower market value of the item. The journal entry to record an impairment is a debit to a loss, or expense, account and a credit to the related asset.

Is impairment loss a non cash expense?