What is Section 280F recapture?

For passenger automobiles, section 280F(a)(1)(A) limits the depreciation deduction by listing the amounts a taxpayer can deduct in the years following its purchase. If listed property is not used for a qualified business, the accelerated depreciation deductions will be recaptured under 280F(b)(2).

What is 280F limitation?

Limitation On Depreciation For Luxury Automobiles; Limitation Where Certain Property Used For Personal Purposes. Except as provided in clause (ii), the unrecovered basis of any passenger automobile shall be treated as an expense for the 1st taxable year after the recovery period. …

What is Code section 280F?

26 U.S. Code § 280F – Limitation on depreciation for luxury automobiles; limitation where certain property used for personal purposes. U.S. Code.

What is Section 280F b )( 2?

Internal Revenue Code Section 280F(b)(2) Limitation on depreciation for luxury automobiles; limitation where certain property used. for personal purposes. (a) Limitation on amount of depreciation for luxury automobiles.

What is a section 197 intangible?

Section 197(d)(1) provides that the term “section 197 intangible” means (A) goodwill; (B) going concern value; (C) any of the following intangible items: (i) workforce in place including its composition and terms and conditions (contractual or otherwise) of its employment, (ii) business books and records, operating …

What is a repayment under claim of right?

A Claim of Right occurs when a taxpayer reported income as being taxable in one year, but then has to repay more than $3000 of that income back in a future tax year. Figure the tax for the current year without deducting any amount repaid.

What vehicles are subject to 280F?

Trucks and vans. Trucks and vans are also subject to Section 280F limits. A truck or van is a passenger automobile that is classi- fied by the manufacturer as a truck or van and has a loaded GVW of 6,000 pounds or less.

Are vehicles 1245 property?

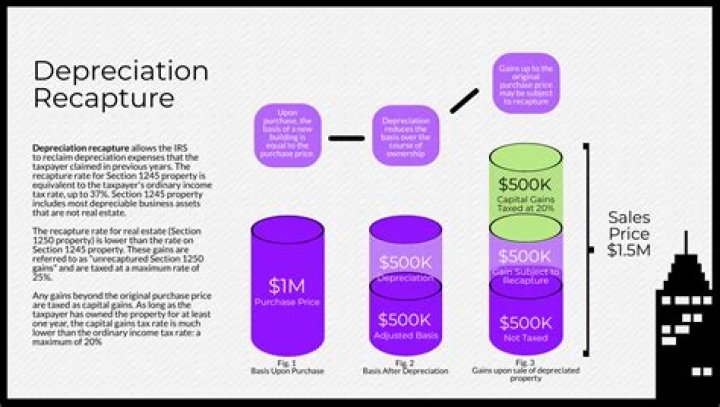

Section 1245 Property is any new or used tangible or intangible personal property that has been or could have been subject to depreciation or amortization. Examples of tangible personal property are machinery, vehicles, equipment, grain storage bins and silos, blast furnaces, and brick kilns.

What is a section 197?

Section 197 of the Labour Relations Act, No 66 of 1995 (LRA) was enacted to change the common law position, with the effect that an automatic transfer of contracts of employment from the transferring employer (previous employer) to the acquiring employer (new employer) now takes place in the event that the whole or …

Are loan fees Section 461?

But the IRS denied the deduction, stating that Internal Revenue Code 461(g)(1) requires loan fees for purposes other than purchase of a principal residence to be deducted over the life of the loan. On their income tax returns they claimed a capital loss deduction for the drilling costs.

What is a claim of right income?

What is claim of right repayment over $3000?

If you paid back income of $3,000 or more reported in a previous year, due to having been paid in error, you can deduct that amount in the current tax year. Also known as a “claim of right,” it is a credit for taxes paid on wages not ultimately received from the previous year.