What is strategic foreclosure?

When breaking even on your mortgage is becoming increasingly out of reach, a strategic foreclosure essentially allows you to cut your losses. It may involve redirecting your mortgage payments toward other debts while building up your cash savings until the bank eventually seizes the property.

What happens when a second mortgage forecloses?

So, if the second-mortgage holder foreclosed, the foreclosure sale proceeds wouldn’t be sufficient to pay anything to that lender. That’s because all the money from the foreclosure sale would go to the senior lender. But the second-mortgage lender could still sue you personally for repayment of the loan.

Is Strategic Default morally justifiable?

As long as Congress is unwilling to force lenders to write down underwater mortgages, many homeowners will conclude that strategic default is not only morally acceptable, but also the most rational course of action.

Do you get money back if you foreclose?

Will I Get Money Back After a Foreclosure Sale? If a foreclosure sale results in excess proceeds, the lender doesn’t get to keep that money. The lender is entitled to an amount that’s sufficient to pay off the outstanding balance of the loan plus the costs associated with the foreclosure and sale—but no more.

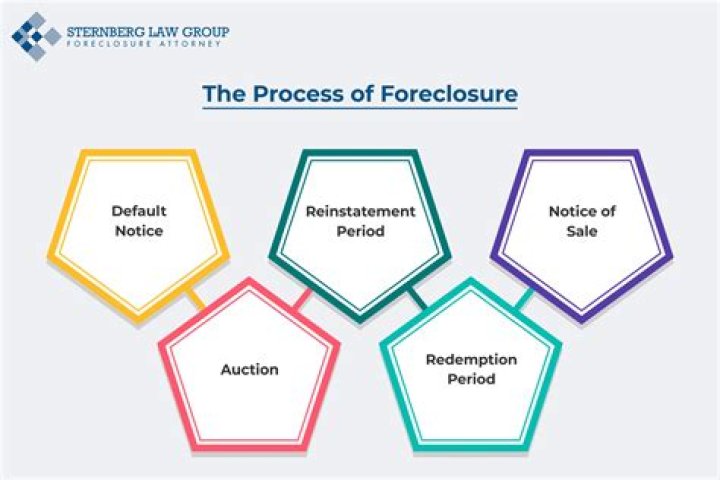

What are the two types of foreclosure?

There are two types of foreclosure: judicial foreclosures, which require a court order, and non-judicial foreclosures, which do not. In judicial foreclosures, the mortgagee must go to court and prove that it owns the mortgage and has the right to foreclose on it.

Can a lender in second position foreclose?

Yes, a second mortgage holder can foreclose, even if you are current on your first mortgage. Just like any type of loan, if you are behind on your payments, the lender has the legal right to take whatever property was offered as collateral on the loan.

Which type of foreclosure is faster?

A power of sale is generally a faster process—usually a few months—for foreclosing on a property, as compared to a judicial foreclosure. So, you’ll most likely lose the property sooner than if a judicial foreclosure happens.

How can a foreclosure process be temporarily stalled?

You can stop a foreclosure in its tracks—at least for a while—by filing for bankruptcy. Filing for Chapter 7 bankruptcy will stall a foreclosure, but usually only temporarily. You can use Chapter 7 bankruptcy to save your home if you’re current on the loan and you don’t have much equity.

What’s the difference between strategic default and foreclosure?

Strategic default commonly refers to the practice of “walking away” from a mortgage. In this sense, borrowers simply stop paying, pack up, and move out, leaving the bank to foreclose on the home. Strategic foreclosure is the practice of getting the bank to take back your home as full satisfaction of your debt.

How does a strategic foreclosure work in Illinois?

In a strategic foreclosure, an underwater homeowner attempts to return the property to the bank. In Illinois, this is commonly done in two ways: a deed-in-lieu of foreclosure and a consent foreclosure. A deed-in-lieu of foreclosure is used before foreclosure is filed.

What does it mean when you walk away from a foreclosure?

This is known as strategic default, which is sometimes called voluntary foreclosure or “walking away.”. Generally, the term “strategic default” implies a different a situation than a homeowner who is struggling financially and cannot afford to keep paying the current mortgage payments.

How does a foreclosure affect your job prospects?

Stigma of Foreclosure. While foreclosure has lost much of its social stigma, many employers routinely run credit checks on potential employees. Because a foreclosure will appear on your credit report, it could cause issues for your job prospects.