What is the current PMI interest rate?

As of 2020, the rate varies between 0.5% and 1.5% of the loan. You can pay PMI in monthly installments or as a one-time payment, though the rate for a single payment would be higher.

Is PMI required at 80% LTV?

Most lenders require that your LTV ratio be 80% or lower before they will cancel your PMI. When your LTV ratio reaches 78% based on the original value of your home, remember that the Homeowners’ Protection Act might require your lender to cancel your PMI without your asking.

What is the 80/20 rule in mortgage?

Essentially, an 80/20 mortgage is a pair of loans used to purchase a home. The first loan covers 80 percent of the home’s price, while the second covers the remaining 20 percent. Both loans are included in the closing and will require you to make two monthly mortgage payments.

Do banks offer 80/20 Loans?

There are two basic permutations to this: 80/15/5 or 80/10/10, however, some lenders do allow an 80/20 in which the second mortgage covers the rest of the purchase price with no down payment. Getting a piggyback loan can be a nice convenience to home buyers, as it closes at the same time as the first.

Does PMI go towards principal?

Private mortgage insurance does nothing for you This is a premium designed to protect the lender of the home loan, not you as a homeowner. Unlike the principal of your loan, your PMI payment doesn’t go into building equity in your home.

How do you calculate 80 percent of your home?

Simply put, your LTV is the ratio of how much you owe on your current mortgage loan divided by the current value of your home. So, if your home is valued at $100,000 and your current mortgage is $80,000, your LTV is $80,000 divided by $100,000, which equals 80%.

What credit score is needed for an 80/20 loan?

Qualifying for an 80/20 Loan Generally, only those with a good credit standing, a score of at least 700, can qualify for 80/20 loans.

How do I get out of an 80/20 mortgage?

You also can reduce your payments by convincing your lender to reduce the interest rate or extend the term of the loan. If your 80/20 mortgage rates are higher than current rates, your lender may accept a reduction. Extending the term from 20 to 30 years also will cut your monthly payments.

What is an 80/20 loan?

An 80/20 loan is when a homebuyer takes a conventional mortgage on 80 percent of a home’s purchase price and a second loan for 20 percent of the price. Lenders require you to get Private Mortgage Insurance if the loan-to-value ratio of the home is higher than 80 percent.

How do I choose the right PMI rate for my mortgage?

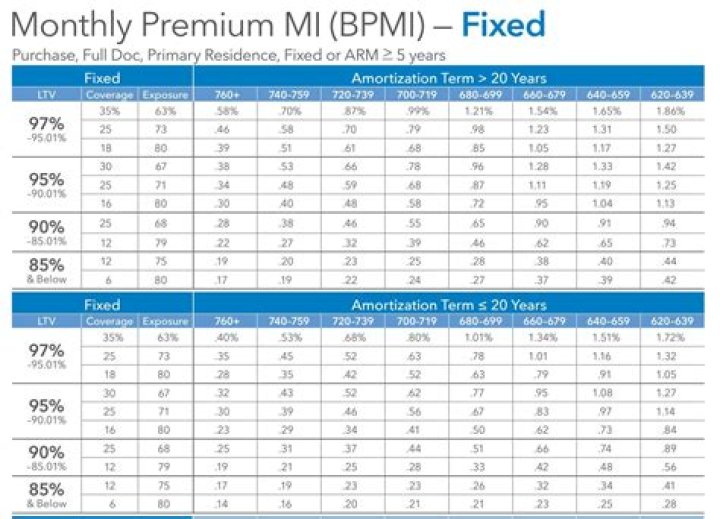

Enter a mortgage insurance rate. When shopping lenders, ask for their typical PMI rates. If you’re not sure what your mortgage insurance rate will be, choose a rate somewhere in the middle of the typical range — 0.58% to 1.86%. Enter a loan term.

What are the risks of an 80/20 mortgage?

The 80/20 may be a little more risky because of variable interest rates and changes in home values. If you end up owing more than your home is worth, or the rate increases too much, you might not be able to continue making monthly payments. Lenders sometimes put a limit on the total amount for the 20 percent loan, such as $100,000.

Do I have to pay PMI on a 20% down payment?

The total amount of PMI you’ll pay until you reach 20% equity. What you’ll pay over the full term of your loan. Your LTV is less than 80%, so you will not need to pay PMI. For conventional loans, lenders typically only require you to pay PMI if your down payment is less than 20% of the loan amount.