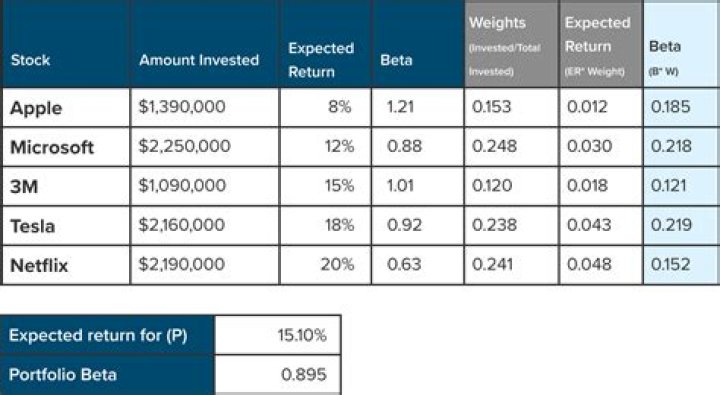

What is the expected return of a portfolio computed as?

The expected return of a portfolio is calculated by multiplying the weight of each asset by its expected return and adding the values for each investment. For example, a portfolio has three investments with weights of 35% in asset A, 25% in asset B, and 40% in asset C.

When a security is added to a portfolio the appropriate return and risk contributions are?

When a security is added to a portfolio the appropriate return and risk contributions are: the expected return of the asset and its standard deviation. the expected return and the variance. the expected return and the beta.

What indicates a portfolio is being effectively diversified?

If a stock portfolio is well diversified, then the portfolio variance: may be less than the variance of the least risky stock in the portfolio. The standard deviation of a portfolio: can be less than the standard deviation of the least risky security in the portfolio.

Which type of risk can not be reduced by adding more stocks to a portfolio?

Systematic risk, also known as market risk, cannot be reduced by diversification within the stock market. Sources of systematic risk include: inflation, interest rates, war, recessions, currency changes, market crashes and downturns plus recessions.

Does increasing the number of stocks in a portfolio reduces market risk?

True or False: Increasing the number of stocks in a portfolio reduces market risk. Consider two stock portfolios. Portfolio A consists of four different stocks from firms in different industries….

| Company | Industry |

|---|---|

| Saalvo | Automotive |

| GMW | Automotive |

| Honsubishi | Automotive |

| Shexxon | Oil and gas |

How is the optimal risky portfolio identified?

The optimal risky portfolio is found at the point where the CAL is tangent to the efficient frontier. This asset weight combination gives the best risk-to-reward ratio, as it has the highest slope for CAL.