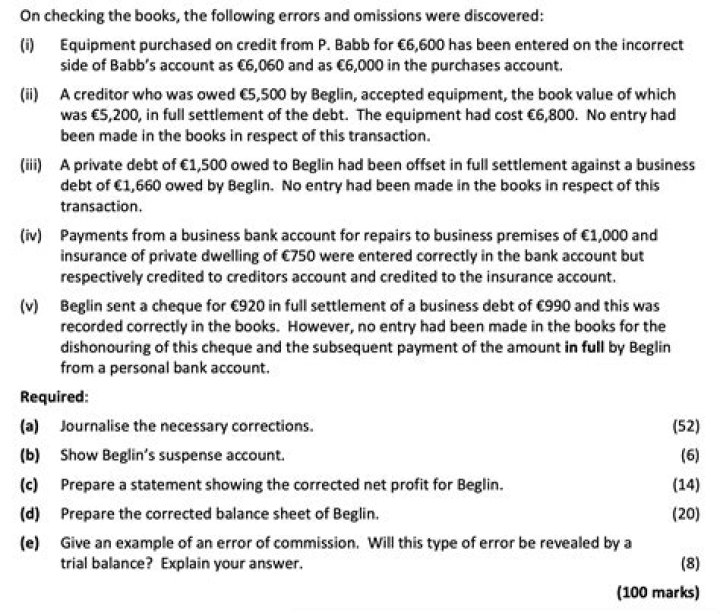

Which entries are passed to make the correction of errors in accounting?

We can rectify these by passing a journal entry giving the correct debit and credit to the accounts. In order to rectify an error, we need to cancel the effect of wrong debit or credit by reversing it and restore the effect of correct debit or credit.

How do you rectify errors in accounting?

The errors can occur both on the debit and credit side of the account and need to be corrected or rectified by passing a journal entry to correct the debit and credit. An error can be rectified by reversing the impact of wrong entry on debit and credit side and restoring the correct debit and credit entry.

What are the rectification entry?

Rectifying entry means an entry passed to correct the error committed.

For which type of errors journal entry is required for rectification?

two sided error

Answer: For which type of error, journal entry is required for rectification two sided error. Explanation: All two-sided errors, i.e. the errors that affect both the accounts simultaneously, are rectified by passing a Journal entry, even though it may be located before or after the preparation of the Trial Balance.

What is rectification entry which entry will you include in this?

Rectification Entry for Errors of Principle A building is a fixed asset hence it should be entered in the building account. Therefore, we will have to rectify the sales account by debiting it and crediting the same amount to the building account.

What is the correcting entry method?

What is a Correcting Entry? A correcting entry is a journal entry that is made in order to fix an erroneous transaction that had previously been recorded in the general ledger. For example, the monthly depreciation entry might have been erroneously made to the amortization expense account.

What are the steps for rectification?

The following three steps are taken to rectify the two-sided errors:

- Identify correct entry.

- Rewrite wrong entry.

- Find rectifying entry by making adjustment of correct entry and wrong entry.

What are the types of rectification of errors?

Types of Rectification of Errors

- Errors of omission: These errors occur in cases like when the entire transaction has been omitted from the books of accounts.

- Errors of commission: These errors happen due to any wrong committed by the accountant.

What do you mean by rectification error?

Definition: Rectification of errors is a procedure of revising mistakes in the entries. These errors can be of two types, i.e, the errors committed on both sides in an entry that does not influence the trial balance and can be rectified by making a journal entry.

What are the different types of errors in rectification of errors?

What is rectification of errors and its types?

What correcting entries affect?

Correcting entries ensure that your financial records are accurate. With correcting entries, you adjust the beginning of an accounting period’s retained earnings. Retained earnings include your take-home money after paying expenses for the period. These kinds of entries are called prior period adjustments.

What is rectification of errors in financial accounting?

Financial accounting deals with recording and maintaining every monetary transaction of an organization. However, sometimes, a few entries might be either incorrect or used at the wrong place. In financial accounting, the process of correcting such mistakes is known as Rectification of Errors.

How do I rectify account errors?

Such errors are rectified by adding a note in account or by passing a journal entry by creation of a Suspense account. The process of rectification is as follows: Identification of account having error.

What is rectification of errors that influence the trial balance?

Rectification of errors that influence the trial balance occurs on any one side of the trial balance and such errors can only be rectified by passing a journal entry along with opening of a suspense account. Such errors are also known as one sided errors as it impacts only one side of the account (either debit or credit).

What are the different types of errors in accounting?

The errors are broadly classified into two types: Rectification of errors that do not influence the trial balance include errors that involve errors on both sides of debit and credit and can be rectified by passing a journal entry. These errors impact two accounts simultaneously and are therefore known as two-sided errors.