Why are contingent assets not Recognised?

According to the accounting standards, a business does not recognize a contingent asset even if the associated contingent gain is probable. A contingent asset becomes a realized (and therefore recordable) asset when the realization of income associated with it is virtually certain.

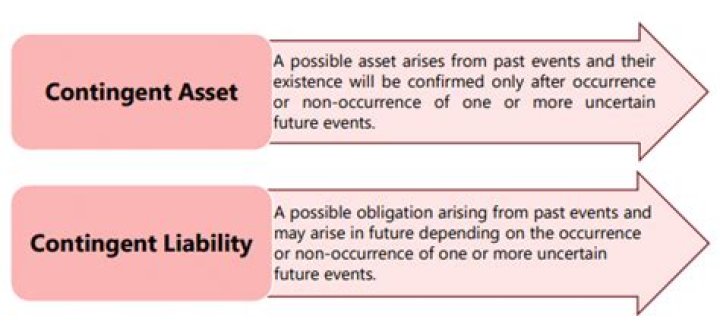

How do you identify a contingent asset?

A contingent asset becomes a realized asset recordable on the balance sheet when the realization of cash flows associated with it becomes relatively certain. In this case, the asset is recognized in the period when the change in status occurs. Contingent assets may arise due to the economic value being unknown.

Are contingent assets disclosed?

Contingent assets are not recognised, but they are disclosed when it is more likely than not that an inflow of benefits will occur. However, when the inflow of benefits is virtually certain an asset is recognised in the statement of financial position, because that asset is no longer considered to be contingent.

What are the example of contingent assets?

An example of a contingent asset (and its related contingent gain) is a lawsuit filed by Company A against a competitor for infringing on Company A’s patent. Even if it is probable (but not certain) that Company A will win the lawsuit, it is a contingent asset and a contingent gain.

How are contingent liabilities calculated?

First, it must be possible to estimate the value of the contingent liability. If the value can be estimated, the liability must have greater than a 50% chance of being realized. Qualifying contingent liabilities are recorded as an expense on the income statement and a liability on the balance sheet.

Has IAS 37 been replaced?

The new IFRS will replace IAS 37 and apply to all liabilities that are not within the scope of other standards. liabilities arising under contracts that have become onerous.

Is IAS 37 still applicable?

The amendments published today are effective for annual periods beginning on or after 1 January 2022. Early application is permitted.

What replaced IAS 37?

IFRS

The IASB issued exposure drafts in 2005 and 2010 that would have replaced IAS 37 with a new IFRS or made significant revisions to IAS 37.

Why do contingent asset recognized only when virtually certain?

Generally accepted accounting principles (GAAP) requires a note disclosure in financial statements for any contingent assets. However, when the inflow of benefits is virtually certain an asset is recognized in the statement of financial position because that asset is no longer considered to be contingent.”

Why contingent liabilities are not Recognised in the balance sheet?

Contingent liabilities, liabilities that depend on the outcome of an uncertain event, must pass two thresholds before they can be reported in financial statements. If the contingent loss is remote, meaning it has less than a 50% chance of occurring, the liability should not be reflected on the balance sheet.

When is contingent asset not recognized in financial statement?

Para -32- Contingent assets are not recognised in financial statements since this may result in the recognition of income that may never be realised. However, when the realisation of income is virtually certain, then the related asset is not a contingent asset and its recognition is appropriate.

Which is an example of a contingent asset?

A contingent asset is an asset that depends on some future happening that may or may not occur. Its existence or value is not assured. A contingent asset may arise from a contigent liability. Contingent assets are not recognised in the statement of financial position.

How are contingent assets defined in Ind-AS 37?

However under Ind-As these Contingent Assets will form part of financial statements as an extensive disclosure as defined under para 89 of Ind-As 37 and hence the company needs to mention a description about the nature of that asset.

How are contingent assets accounted for in GAAP?

Contingent asset accounting policies for GAAP are outlined in the Financial Accounting Standards Board (FASB) Financial Accounting Standard Number 5. Companies must reevaluate the potential asset continually. When a contingent asset becomes likely, firms must report it in financial statements by estimating the income to be collected.